The economy is a mess and many young people are struggling more than they would like to admit. It is during times like this that men are offered an opportunity to awaken their masculine virtue to triumph over their materialistic world. When scarcity hits hard, men will either falter and become trapped in a cycle of financial and moral poverty or use the challenge as a means to actualize their potential.

If you are strapped for cash or are looking for ways to save more money, consider choosing a minimalistic lifestyle to maximize your potential. Try following the tips below to invest your limited resources on the one thing that matters most: your life.

1. Keep A Personal Financial Record

The trick that helped me curb my foolish spending spree was to keep a record of my finances. As they say: What gets measured, gets managed. It is very simple to do and it will help you keep track of where all your cash is going. To do this, on a notebook or a spreadsheet program, record and list all your expenses and income for each month (it’s much easier and efficient if you round everything to the nearest dollar). And at the end of the month, total up your income and expenses to see just how much you’re spending and saving. After tracking your finances for a while, you become conscious of your own spending habits and learn to restrain when necessary.

2. Put Value On Experience Over Pleasure And Status

It’s simple: The money you invest in creating experience and value for yourself will stay with you for life; buying for pleasure and status is shallow and will not last long. Good places to spend your money on are knowledge, skill, health, strength, business, and other ventures. Don’t be the fool spending money on vanity.

3. Buy For Utility And Durability

Objects are just objects, and unless you apply some non-existent value mentally, its only value is in what you can do with it. For example: a Rolex watch does the exact same thing that a cheap watch does, so what’s the point of dishing out a large sum of cash for something that does the same simple job? Always think in terms of utility and durability. Nothing else really matters.

And although you want to save money by not wasting it on luxuries, note that buying something cheap isn’t always the best option. Buying cheap may save you money instantly, but it may cost you in the long run when it starts to break down and become a useless junk. Sometimes, you need to invest more for the quality and durability.

4. Never Buy Anything On Credit

This is not to say that you should not use credit cards, but rather than you should never buy something with a credit card that you cannot pay off in full each month.

I personally never buy anything on credit. When I need something, I buy it when I have the money and pay everything up front. The idea of enslaving myself with debt is so ridiculous to me that I can only shake my head when I hear about people getting a new television set—which they can barely afford—with monthly payments.

5. House And Car

These are the two biggest money drains that shackle people. Depending on your location and job, having a car might be something that is necessary. Home ownership, on the other hand, has long proven to be a scam. After witnessing what others put themselves through just to keep a home, I know I would always rent rather than be a mortgage slave.

6. Opt For Calisthenics And Basic Equipment Over Gym

Another place you can save an extra cash is by canceling your gym membership for body-weight training. With calisthenics, you don’t have to get a long-term membership and you don’t even need to commute. You can do all your workout at home with just basic equipment like a fitness mat and a pull-up bar which are cheap and easy to obtain.

Yes, calisthenics isn’t likely to get you the same results as working out in a gym, but if you just want a decent workout that will also help with your balance and flexibility—and with less chance of injuries—then calisthenics should be fine for you.

7. Avoid Drinks You Don’t Need

The only drink you really need is water. Besides the occasional green tea, I don’t ever see the point in wasting money on other drinks and beverages.

I never felt the need to drink coffee—I never started the habit and I don’t see any reason to do in the future. It’s strange for me to see bunch of cranky people at the local Starbucks or Tim Horton’s line up for a cup of coffee in the morning like zombies. I think many of these people vastly underestimate the importance of sleep and should really find ways to invest more of their time to it than looking for their fix of caffeine on a daily basis.

Soda is a can of liquid sugar. Nothing more needs to be said. Alcohol is a toxin. I only drink socially and almost never more than a beer. They’re too expensive for the little to no value they provide. But of course, just how much you decide to drink will vary widely depending the lifestyle that you choose.

8. Avoid Unhealthy Snacks And Junk Food

Not only are they a waste of money, but they’re often detrimental to your health. Either get healthier snacks like nuts and fruits or just wait until your meal time.

9. Cook Your Own Meals

Eating out can be convenient, but costly. Learn to cook healthy meals for yourself and save money.

10. Get Off The Screen

You’re a man, you have better things to do than to be “entertained” in front of a screen. Stop throwing your money and time away on movies, television, video games, porn, and what not. (And don’t even get me started with sports fans who buy expensive jerseys with another man’s name on them.) Cancel everything and get rid of them all. There are so many other meaningful things you could be doing with your life.

11. Phones And Other Electronics

Nothing says consumer culture gone mad like the sight of sheeple lining up in front of Apple stores for the latest version of the iPhone that does the exact same thing as the one they already own. Who could have predicted that planned obsolescence would go so far?

Phones and other electronic devices have become the most vapid status symbols of our age. Just get a decent device that will do the job for years to come, and stop placing the value of electronic products above your own individual self.

12. Ditch The Poo

The human race gave gone along just fine without a shampoo until about some decades ago. Shampoo is essentially a chemical toxin that destroys the natural oil in your hair, prompting you to use another chemical product—the conditioner—to restore your damaged hair. It’s the perfect business.

Roosh himself posted the result of his experience of not using shampoo and I myself have gone from using it twice daily to none at all with great results. I can say for certainty that my hair now is much healthier than ever before in my adult life.

13. Limit Your Clothes

I’ve met men who take their fashion more seriously than a woman. For Pete’s sake, just buy a few things that you need that look good and no more. You’re not a woman, you don’t need to go shopping every week to play dress-ups.

14. Stop With The Decorations

There is nothing more pathetic than seeing men cover up their insecurity and inadequacies with expensive objects. You don’t need jewelries like a woman, you don’t need that tattoo, and you don’t need pieces of “art” scattered around your house. Keep your life simple and invest in yourself instead.

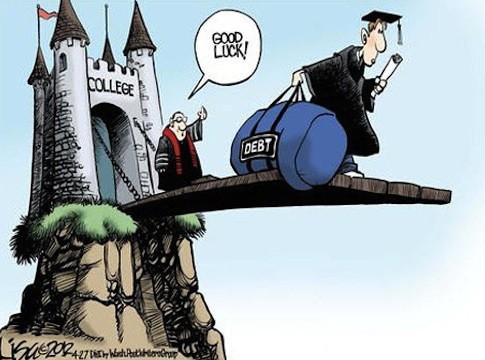

15. Avoid The Education Scam

College is the biggest scam that is oppressing young people today. Anyone who is considering college should check out the student loan debt clock and see if they want to be part of that number. And if you insist, be smart about the path you choose. Your dreams may seem set now, but they’ll pop like a bubble when the reality hits you like a sledgehammer. For all those who are starting to plan out their future, Mike Rowe has a message for you:

16. Feel Free To Spend Money On What Matters for You

The point of saving money, of course, isn’t necessarily to live like a Buddhist monk (although that is a possibility if you seek an ascetic life), the point of it is to prioritize what you truly value in life. With more money, more time, and less clutter to distract you, you will be in a better position to strive ahead towards your goals and ambitions.

Using the tips I mentioned above (minus the fact that I went to university), I was able to pay off all my student loan and save around $10,000 working a part-time job. I would have saved thousands more if I had applied those principles sooner. And I was able to accomplish this within few years of my graduation while living in a meaninglessly expensive hellhole in Canada. While others are still stuck because they blew their money on brainless “fun,” I invested my time and money on self-improvement and I’m now in a better situation than they can ever hope for.

You always have the choice between living for the moment and living for life. Choose wisely.

Read More: 20 Things You Can Do Instead Of Playing Video Games

Excellent self improvement article. I stopped using shampoo about 4 months ago and I’m not going back. For those who want to pursue their education without dropping a wad of cash, go to coursera.org. They provide free courses from universities all over. Don’t think you get any official certificate but you will get the knowledge.

I’ve actually just started using a credit card for the cash back perks, but I have the money in the bank to pay it off each month and I only use it on necessities I was going to purchase anyways like groceries.

Now about that house mortgage….that’s an area that still needs work.

With regards to the mortgage, if you can, refinance to a shorter term and lower rate and consolidate all debts into this lower rate. Pay extra into principle and have a plan on when this will be paid in full. Stay disciplined in your plan. Add more to principle if you can swing it to accelerate the pay off date.

One way to keep motivated in paying off the debt is to look at the interest you’re paying each month. That should be a wake up call right there.

We’ve already refinanced and used our tax return to pay off quite a few grand in bills. My wife and I have decided 2016 is the year we really knuckle down and start chipping away our debts. Going to be harder for her than me since I’m content living on a minimalist lifestyle.

Well, fuck it, I’m gonna have to toss the shampoo then. Seems like a lot of guys have discovered that it’s BS.

My dad doesn’t use deodorant. He also doesn’t stink or really smell bad and works outdoors all the time. I’m starting to think a lot of this shit we put on our bodies is bad for us.

research vaccine injury and vaccine side effects, some of the most toxic things we consume are put inside our body!

I dropped shampoo two years ago and I’ve never had better feeling hair. I’ve also switched to baking soda as my deodorant and stopped using soap unless I’m actually cleaning off something disgusting. For regular cleaning just scrub all over with a shower cloth.

Shockingly, our bodies did not evolve to be dependent on an assortment of manufactured goods to survive. Fancy that!

I am going to move in this direction. Also, baking soda is amazing stuff! My dad uses it for toothpaste, although the taste is a little odd and it has a different, kind of gritty feeling in your mouth, but works well. How do you apply baking soda to your armpits?

I keep a 4oz tupperware container of baking soda in the bathroom. After a shower, wet your fingers under the tap then pick up a pinch of it. Rub it around on your fingers until it turns to paste (sometimes need to add a bit more water from the tap) and then rub it on your armpits.

A word of warning: When I started doing this it irritated my skin. A week or two in and it stopped having any negative effect. Also when it’s wet it’s easy to get it on your clothes. It doesn’t stain, but it leaves you with a line of white dust on your shirt that people will comment on. To avoid that I usually wait 10 minutes or so before getting dressed to let it dry out a bit.

Gotcha. I have stopped using the “aluminum” based deodorants. An older coworker who has now passed pointed out to me that they cause “hard pits” — the crusty hardness that develops on the clothing of your armpit–I especially noticed this on all my undershirts. The only reason I haven’t gone full baking soda is I understand it’s a deodorant, but not an anti-perspirant, and I don’t like the sweaty, wet feeling of armpit sweat. Although it’s pretty unnatural to clog and force your skin cells to stop sweating, which is what anti-perspirants do.

I use shampoo only if I get dirty from the factory I operate, but that’s only when I get in intimate contact with the refractory wool blankets. Those fibres don’t come out any other way!

So is Roosh still not washing his hair?

I love people who doesn´t buy properties and thinks that is a scam.Please, live on a rent for your entire live it´s the best thing you can do…i can say only, thanks for making me richer every day.

Heard a story about a property investor who sought out a space a year ago. It was a fixer-upper but only really required the kitchen to be modernized and a few walls layered and insulated. The space was originally 400k. A year later, Google moves in nearby. The property of everything in the area doubles, including the loft. Now worth a healthy 800k, the owner sells and walks off into the sunset. How long does it take to earn 400k again? Not counting taxes, average investment options, income levels, and cost of living expenses.

If you look into the numbers its probably a lot less than $400000 profit.

And of course house prices never go down, right?

Cost to sell, yeah, there is a net loss. But there should be at worse a net gain of at least 100k, which is still sizable enough to try and flip that investment into something else. The main draw was the luck of having Google become the next door neighbors.

they didn’t understand that the tip is to buy properties and put people in there, not living in.

You should go contrary opinion with the corporate matrix, if it says buy a property then rent, now they say rent then you have to buy.

Very good article overall, but number 10 (Get Off The Screen) is hardly working against saving more money.

Quite the contrary, downloading movies, music, tv shows, (or porn for that matter) for free off of torrent sites will save you a boatload of money over time rather than getting off your ass and repeatedly purchasing physical copies of those things or frequently going to the movie theater (unless it’s a date or big social occasion).

I read #10 as use your mind and time in a more proactive manner. When you “watch” you are in the act of consuming. Read, write, think, talk to your other, play games and you will find your frame of mind much swayed away from consumming shit on a screen created by someone else to get your money or soul.

Correct. Many people still go to the movies, go watch sports, pay for Netflix and music, etc. They drain both money and time.

I only have Netflix but usually only watch it while doing something else. I’m one of those guys that needs something going on in the background while I work. Agree that most people spend WAY too much on entertainment though. I know some people that have cable, Netflix, Hulu, and go to the movies a couple times per month. Talk about a lot of money going down the toilet for the exact same activity.

just get Apple TV and set up a network..

One thing that I got for Christmas that I really like is Google Chromecast. It hooks into your TV and you can play anything from your iPhone. I’ll usually stick on a YouTube or Netflix video while working around the house. The Chromecast doesn’t charge a monthly subscription or anything so it’s nice in that regard.

now we have hulu, netflex, or amazon prime. You can select want you want to see and not to see.

I’d add: get rid of pets, cable TV, bodybuilding supplements, health foods, and high-maintenance women.

press magazines too. always the same recurring shit, isn’t worth the money spent

I’m slowly dwindling down my pets. We started with 3 dogs. One has since died and I’m adamant about not replacing her. I already told my wife I don’t want anymore pets until the current batch run their course.

Planning on growing a lot of veggies this spring as well.

My take on animals: if you can’t eat it, dump it. Unless it’s a big dog that will watch your back.

One is a lab mix, so pretty big. The other is a miniature schnauzer. I normally shy away from smaller breeds, but mini schnauzers are pretty damn manly…I mean c’mon! They even have an epic beard.

They look like everyone’s grumpy old neighbor who tells you to get the fuck off his lawn.

And speaking of German breeds (seriously, what’s up with Germans and their awesome dog breeds?) if there was one small breed I would keep, it would definitely a Dachshund. Fierce little bastards.

Nah, no grumpy old man yelling at kids to get off his lawn has a beard like this. I’ve never been a fan of the Dachshund.

From what I’ve been told, Germans have a propensity towards efficiency so it may have influenced the types of dogs they bred. I don’t know enough about the 2 breeds we’re discussing to make any kind of speculation. I like to think the Germans were sitting around one day and said, “You know what? We need a dog that looks like he should be smoking a pipe. Brilliant!”

Believe it or not, we did have a neighbor that looked just like that. In fact, he looked like the love child of a Schnauzer and Rasputin. Nobody ever came close to his house because apparently the guy harvested children’s organs, or that’s how the rumor went. And he was one of the few persons in our neighborhood with a decent lawn, so he got pissed anytime someone stepped on it. But yes, gotta love the Germans and their way of making a good animal even better. Better than the French and their poodles anyways.

My favorite joke about poodles was on NCIS: LA…someone said, “Ah yes….Poodles. France’s pitbulls.” Love France, but that was funny.

As a Poodle, I find that extremely offensive.

Hah, as I was typing this I was thinking to myself “Wonder if Monsieur de Charette will stumble across this comment?”

My neighbour has those dogs, got bitten twice by them. They are aggressive little twats

Obviously you have never seen a standard poodle. They are classed in dog shows as a working breed, and are large, emotionally stable, and good with kids. A typical one is about waist high or higher on me and I am 6’2″. They screwed up the breed, as they did many others, when they minaturized them to be lady’s lap dogs.

They were created to be water retrievers. The hair cut was to minimize the amount of water absorbed in their fur while keeping their joints warm. It was all practicallity and business.

My dog rounds up my sheep which I graciously eat

I’m waiting for the day Monsanto shoves thru congress that we can no longer grow our own vegetables…thats when we know the dark ages are almost nigh.

Chief, unfortunately, this is already the case, these laws are already on the books, it’s just not time for them yet.

There have been a few oldies arrested already of growing in their front yards.

Check Out Codex Alimentarius, anything not grown by a corp will be classified a neurotoxin.

My family is doing this now. I care for my elderly mother an we have one dog left. We might take my sister’s elderly dog in to make sure he’s cared for properly.

Beyond that not another animal. Maybe if we buy property in the country a dog to watch the property would be nice. Beyond that no more pets.

“Grow your own food” should be on this list. However it is harder to have a yard to do this if you’re renting.

I always poke fun at owners of exotic animals like pythons. Besides the legal, personal, and environmental risks that these animals possess, they’re just plain boring. If they’re not suffocating tiny little bunny rabbits, they just sit there. And it’s not their fault. That’s how nature made them. Definitely not worth the cost. And horses, meh, they’re good for stew.

Wherever you see someone who owns a horse you see someone who is broke, usually to the point of being homeless, from owning a horse.

I don’t get the appeal.

health foods are not a waste of money. An organic tomato has more nutrients than five non-organic tomatoes.

Agreed for the rest. A guard dog isn’t a waste either. Ditch the chihuahua

At five-time the cost.

Is it because the tomatoes are organically grown, or just that they are better raised and not franken-farmed, generally? I’m skeptical of a lot of the “organic” crowd claims – a lot of it reeks of marketing hype.

>>pets,

Dogs are your alarm system, and your most loyal soldier in a fight.

I’m a cat person myself but if you plan to live ‘away from it all’, a dog and gun are almost necessities (definitely the gun)

You can have both (cat and dog), as I do. If you live away from it all mice are going to be a problem and cats the most natural solution.

Pets are perfectly fine, once you can afford them.

There’s being frugal, and then there’s being a tightwad. I couldn’t imagine going through life without a dog by my side. It’s not like the wife is going to go chase down the ducks I shoot. God knows I’ve tried to get her to do that, but, well…

People should be making kids not adopting animals.

Agreed, Pets are good as part of a family once a men decides to settle down but I dislike the USA culture of pet worship…

❝my .friend’s mate Is getting 98$. HOURLY. on the internet.❞….two days ago new McLaren. F1 bought after earning 18,512$,,,this was my previous month’s paycheck ,and-a little over, 17k$ Last month ..3-5 h/r of work a days ..with extra open doors & weekly. paychecks.. it’s realy the easiest work I have ever Do.. I Joined This 7 months ago and now making over 87$, p/h.Learn. More right Here!b949➤➤➤➤➤ http://GlobalSuperEmploymentVacanciesReportsReview/98$hourly…. .❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:❦2:::::!b949….

cats keep the mice away. plus, well, cats are awesome. if you’re not manly enough to recognize that, i pity you.

You can even train your cat. Mine gives his paw, stands up and jumps on my shoulder from the ground (when there is chicken at stake).

The ideal is to have both a cat and a dog.

that’s awesome.

Most cats are kept in ways counter to their nature. My sister moved to a cabin near a lake and was irritated by the volume of varmints she had to deal with. She got a Siamese cat from the same litter as my father did. She never fed the cat. It lived or died on its own hunting. When it matured it was one mean, badass cat, and solid muscle. It tore up the German Sheppard next door (not that close) on a regular basis. It took good care of the mice and even the larger rats, muskrats, squirrels, and some larger critters. The only problem from my sister’s perspective was that the cat also killed all the birds that came anywhere near. Meanwhile, my father had his declawed and kept it indoors. The cat was fat, lazy, and good for nothing; just like American women.

I agree with this, though would change to “cut back on pets”, and would add:

If it is something of a long term investment such as a sidearm, work equipment (like a tractor), tools (e.g.: Craftsman), a good razor, etc., then buy quality, even if it costs a little more the reliability and maintenance is an overall cost-savings.

Cheap tools always cost more than quality tools in the long run.

I have a broadcast TV antenna and I am perfectly happy with it. It have a cable modem for internet so I can watch what i want on Netflix if I absolutely need to see something.

You can buy a barbell set and rack for $200. I did it. Simple.

As for renting vs buying a house: Pay $8000 per year in rent is a lot better than paying it (mainly interest to a bank) on a house. At the end you still have responsibility for a house, extra costs, and the principle to pay.

As for paying the landlord— he gets your rent and pays 50% in taxes as its income. Its not as sweet of a deal as it looks.

My landlord covers homeowners association fees, taxes, etc. I just live in an apartment for a rent lower than the avg mortgage/sq foot of any condo or house in the area.

Life is good.

I’m torn on the rack. I have one at my house, but rarely use it opting for bodyweight exercises and martial arts instead. I might start using it again for squats, but that’s about it.

I’ve been playing with the idea of creating a weighted sandbag out of an old army duffle bag to lift/throw/carry. To each their own…I’m a variety is the spice of life kind of guy so I typically flit from one exercise style to the other.

This is very important to mention.

In case you were wondering, the economy along with the banks are about to collapse once again, except this time, it is going to be worse. Due to the public outrage of the “too big to fail” banks being bailed out by the tax payers, this time the banks will be “bailed in” meaning that the savers and depositors will be liable to pay for the damage. Here is proof:

United Kingdom:

https://www.gov.uk/government/consultations/bail-in-powers-implementation-including-draft-secondary-legislation/bail-in-powers-implementation

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2015/q302.pdf

United States:

Frank Dodd Act: Title II

I have mentioned this before but it is worth bringing up again.

As I write this, we are living in very uncertain times. The shape of the economy in conjunction with everything else happening in our world, has led us, as a civilization to a point in which the remainder of our future is in a questionable state. The truth of the matter is I don’t know what exactly the future holds. However, with that being said, I can be certain of the fact that it does not look good but rather bleak.

We all know and have heard about the conspiracy theories that we hear from time to time. But rather than delving into that realm entirely, I would rather pick out certain coins from the conspiracy well, which are unfortunately, coming to fruition and proving to be true. The gravity of the current circumstances in which we find ourselves in, is turning to a point of financial disaster. In fact, some of this is already happening and taking place in many different countries around the world:

-Negative interest rates.

-Bail ins.

-Abolishing of cash.

-Confiscation of gold, silver and precious metals.

When reading all of this, without a shadow of a doubt it would make you angry and question the legality of these actions that will take place across the world. But I assure you that from studying all of the relevant legislation that have already been put in place and ready to be fully implemented when the time comes, you will have no choice but to cooperate. Remember Cyprus? Many countries such as Sweden, Denmark and Switzerland, have already put some of these measures into place and it will not be long before they come into full swing here in the Western developed nations such as America, Canada and Great Britain. So as an individual, it makes you wonder, what is the point of living then? Why bother getting up from bed and even going to work, if all of my hard earned money, is simply going to be stolen by the banks? Whether or not this was all planned and engineered the real question is what can you do about it?

And the answer is simple- nothing. You cannot change the outcome of the economy. But what you can do, is to change the outcome of your perspective on life. It is only natural that we as men, look towards building money as this provides us with a meaningful purpose in life. It has been the engine of our fundamental existence for a long time. But as I have said, the future is very uncertain. However, with that being said, I suggest that we as men change our focus. Rather than fixating our life’s purpose on acquiring capital, we should instead focus it on a more important commodity and one which is commonly overlooked. It is called time. Time is the most important commodity that we as human beings, have in this world. From the day that we are born, we have all been stamped with an expiry date. We do not know when this expiry date is going to occur but what we do know is that it is indeed

going to happen.

Therefore, rather than treating money as a form of commerce, one should learn to find an alternative form of currency and one which is out of the hands of any form of regulation. That form of commerce is time. When you come to this epiphany, this eventual realisation can be felt like a baptism on fire. It allows us to come to some form of rebirth while at the same time, allow us as individuals to feel reinvigorated and redefined with a better purpose in our life. Now, I’m not saying for you to go “YOLO” and waste all of your money. On the contrary. In fact, this is what the banks want us to do in a desperate attempt to stimulate our failing economy. No, what I am saying is to refocus your priorities in life and to come to the simple understanding that our lives will be coming to an end. Money should really be considered as a means to an end. Therefore, abandon all of the false lessons and principles about what it means to have a so called “fulfilling” life which you were inoculated and

indoctrinated with throughout the education system, and instead, create your

own end goals.

What these goals may be, is entirely your prerogative. But make sure that they help to fulfil the remainder of your lifespan. For some, reading and acquiring new knowledge on different areas of life such as philosophy and science can be this goal. For others, it can be travelling the world, learning a skillset or spending more time with loved ones and friends. But whatever that goal maybe, it is definitely more fulfilling, more accomplishing and enriching than acquiring money ever was. Even as a misanthropist, I have made it my personal mission in life to ensure that I undertake some of these examples which I have given, as my life goals and to remind myself on an everyday basis, that this life will come to an end. Therefore, with all of this being said, I hope that readers will find some comfort and encouragement in what I have said because no matter how much bad news we are hearing on a regular basis, this should not stop you from living your life. The world has been burning down since the very inception and creation of it. But that should only help to serve you with a reminder that life is indeed short, which in turn, should encourage you to go out and live your life to the fullest.

13 is an interesting point. I’d like to see RoK approved male dressing articles on here. I wager fashion is not a concept most of us are very knowledgable in; at least, I am not.

I would suggest visiting ironandtweed.com. Nate discusses fitness and style. Highly recommend his page.

Or http://www.wellbuiltstyle.com

Thanks for the link. I’ll look into it….knave!

You don’t need to follow the latest fashion trend like a faggot. Men’s classic style hasn’t changed much for decades. Be confident in yourself and dress accordingly.

Well to be fair to Marcus, he didn’t say the “latest” fashion. I’m with you that the classic style looks best on most men. Most of the effeminate hipster style is cringe worthy, at best, downright pathetic at worst.

here’s a fashion tip : don’t shove shower curtain rings in your earlobes. You think that shit is gonna impress anyone at a job interview?

One piece of advice: don’t shy away from thrift stores and yard sales. About 10 years ago I was doing roofing at Minot AFB, North Dakota. We hit the base thrift store one day. I managed to find me a nice Nautica jacket that was probably worth $100 retail. How much did I pay for it? $10. To this day I still wear it.

I’d say just buying clothing that fits properly, a nice belt, and matching shoes will put you miles ahead of most guys.

I never realized how terrible my xl dress shirts and baggy khakis looked until I starting lifting again and bought the correct sized dress pants and slim fitting button up and polo shirts.

Hell just throwing away my xl t-shirts and buying larges that are slightly snug has made a huge difference.

17. Avoid the high maintenance women

Guilty as charged.

You can get a gym membership super cheap these days and i’d say that’s in keeping with spending money on health and strength.

Unless you are seriously out of shape, old or injured, bodyweight excersise doesn’t cut it. you need to be lifting weights.

The best way to save money is to be really smart, and not a woman. Smart people get a bigger rush from making money than spending it, and tend to have greater requirement for intellectual stimulation than the material and earthly pleasures.

The weak and the stupid want to have things. The smart and strong want to BE and DO things.

I dunno, there’s plenty of prisoners denied access to proper gyms (and have shitty diets) who still manage to stay in insane physical condition.

17. Drive Uber around the rich part of your town. 18. Only sleep with rich milfs, while their husbands is out for a business trip. I mean you dropped him off at the airport, anyways.

Sound solid advice. Also check out Dave Ramsey and his 7 Baby steps.

I pay $10 a month for my gym and it has everything I need, so I don’t consider it a waste. If you want to put another item on your list, it’s the state lottery. Talk about throwing away your money, especially with some states selling $50 scratch tickets.

Considering how ironic it is that they’re going after fantasy sites FanDuel and DraftKings for considering it gambling, state lotteries are a big racket in themselves.

No argument there; I live in California and I really wish they’d shut the damn lottery down. I’m all for freedom of choice, but I really fucking hate the lottery. Though it does serve a noble role in funding education and other public programs.

And even then, I hear some states like Michigan have squandered lottery earning on who knows what while schools start breaking down.

I understand the rationale but I still worry about men ditching college. An educational underclass is unlikely to win the day. Allowing for fact many may be better off going into a trade etc for the rest the point should be about being discriminating in choosing how one educates oneself. The danger of indebtedness should however be considered very carefully

Unless it’s a STEM field you can get an equivalent or better education for the price of a library card.

Certainly focus on STEM. But beyond that what you get through self study may not buy you access to jobs or institutions. Lot of crap degrees that will get you little more than a mcjob but you could overestimate the extent to which that is the case

You can also add learning to fix things on your own. Home appliances and cars are pretty easy of you’re handy. The internet provides useful information on how to and save money on parts if they need to be replaced.

I’ve seen a resurgence of shaming men for not having basic DIY skills in the form of memes. Raises my hopes that we might see a return of masculine values.

Outside of changing a tyres or an oil change, try fixing the engines on modern cars/trucks…..the manufacturers make sure you have to go back to them to get a service…..

Yeah, I don’t like newer cars. No space under the hood to work. My first car was a ’78 Plymouth Volare with holes rusted clear through it. I got a crash course in using bondo, priming, sanding, and painting, working on the carburetor, and replacing the alternator, on top of the basics (tires/brake pads/oil/etc).

Actually they’re not as awful as you’d think. I grew up gutting old cars from the ’40’s through the ’70’s (the car model year, not me being 80 years old, heh), and yeah, they were easier. I’ve talked to some modern mechanics and they’ve told me that the computer work is really not that big of a deal, most of the time you’re just monitoring for a voltage level and that’s it (1.7 volts I think?)

Agree. A lot of the times, it’s emission stuff. Get a good OBDII scanner and multimeter. Use the internet to help you diagnose the issue. Chances are someone had the exact same problem you have and posted a YouTube video how to fix it.

Shop OEM parts from a car dealership outside your state. Dealership parts departments have online pricing much lower than retail. Take that quote and go to your local dealer and have them match it or come close. That way, you get the part you need right away and you could return/exchange if there’s anything wrong with it.

Exactly. The OBDII and associated electronics combined with what information is available nowadays takes a lot of the guesswork out of your average repair.

I would approve of that IF, and this is a big IF, there was a coinciding movement shaming women for not being feminine.

“Men, if your “woman” can’t cook a fabulous meal, keep in shape and not curse like a sailor…..

You’re actually sleeping with a man…”

Baby steps. If we can get more REAL men, the women will naturally want to adopt the feminine role. If that doesn’t work, then we pull out phase 2.

Nice try….almost any car built after 2000 is so filled with computers and circuits that you need to be a software engineer not to FUBAR the thing by poking around. I rented a car a few years back and spent 10 minutes trying to find where the ignition was on the steering wheel…I finally got the desk agent to show me the BUTTON you press to turn on the car!

And what, pray, is “phase 2”?

It’s pretty strange, no doubt. But I don’t think it’s as bad as you think. Look at mechanics in a shop and tell me that they’re software engineers? Nah, they aren’t. You just need a couple of specialized tools that I can’t be arsed to purchase.

My motorcycle on the other hand I’ll strip down to individual molecules and reassemble, if it gets cold and boring enough in winter.

Live eels and duct tape.

It’s not as intimidating as it seems, but you do need to do your research before you tinker. Plenty of good vehicle specific forums out there for information.

One doesn’t have to be able to fix anything, and even if machines were at their simplest that would still be pretty involved.

But every guy should be able to fix most anything around a house that requires basic tools, and even a basic remodel of a small room should not be outside of a man’s abilities.

I remember fondly my first car, a Chevy Biscayne. It was a straight 6, three on the tree, AM radio only, no A/C, and no seat belts (none of the cars made in the US had them at that time). You opened the hood and you could sit on the wheel wells and dangle your feet down the inside of the engine compartment. I did almost everything to that car myself. In those days you needed to do a bunch of maintenance, and quite often. Changing spark plugs, setting the distributor point’s gap, and rebuilding the carburetor were common events. Nowadays these things are once every thirty thousand miles, if then. When I got my new 1990 Lincoln Towncar I asked about the maintenance schedule and they told me to bring it in at 100,000 miles whether it needed it or not.

I do agree about the beauty of motorcycle maintenance.

I owned several bikes before I had my major accident (damn four wheel female idiot driver, but I repeat myself) and stopped riding, as I had children for which I was responsible. Anyway, I can truthfully state that I have never bought a motorcycle that was in working condition when I got it. Working on the bike is half the fun.

I don’t have any eels handy, will duct tape alone be sufficient?

The maintenance schedule on new cars is insane isn’t it? Not complaining, but it does take a lot of incentive out of “do it yourself” when you don’t need to twist a wrench but once every ten years or so (oil/tires/filters excluded).

I’m with you the motorcycle man. Such a simple machine unmuddied by so many accessories when it comes to the basic engine. A V-Twin is maybe the most ideal engine to learn on, in my estimate. That so many riders are Corporate Sponsor Riders that don’t do their own maintenance is a damned shame. In my circles if your bike hasn’t been broken down in your garage at least once in the winter, you just aren’t a serious rider.

Not being able to do engine work isn’t fair depending on the vehicle’s make & model.

That being said I just bought my first mechanics tool set so I can start doing basic work on my own. My brother and grandmother will need their starters replaced this summer.

Adding on to your point, what you can’t fix, like, say, a head gasket in a car engine, at least do your research, so you don’t get stiffed by a shady mechanic.

“Wealth consists not in having great possessions, but in having few wants.” –Epictetus

Ain’t that the truth!

17. Avoid women.

Never, ever buy on credit because it will be repossessed if you land in a hot shit and can’t make the payments. Also, you will pay consierably more if you buy on credit.

Also, make your own meals and that will be healthier, cheaper and allows you to save money if you pack a lunchbox.

ETC ETC…. I don’t like spending money because I have to work hard to make the same amount again.

One thing that really changed the way I view finances is I estimate how long it takes me to earn the money to pay for the item in question. That meal at the restaurant would cost me 4 hours of my life…nope, fuck that.

See how easy it is.

If your hours are worth more $$$, then the equation can work the other way. It may be cheaper to pay someone else to make lunch for you…

Always save money. Always. Make it your top priority when you budget.

Some of the best advice I heard from my senior year in college (not that I needed it, but the rest did) was to live within your means and save FIRST. Professor pointed out that you are all probably living on $10k a year or less right now, which of course was true. Whatever the dorms cost plus our meal plan was well under $1,000 a month.

He said remember this minimal living style and postpone any major purchase for a year. Most people easily move up to spend any disposable amount of income. IE if you get a $30,000 a year job, you will quickly move up to a $30,000 a year lifestyle, when EVERYONE is getting by fine on a $10k a year lifestyle now.

He also said to postpone any major purchases by a year and save that money. Instead of buying a car, wait one year and buy it later, you will have saved ( up to $20k in this example), plus that money can compound if you save and invest it.

All very good points however I would disagree with the sentiment that owning a house is a scam. The real scam is a mortgage. You don’t own the property if you have a mortgage, the bank owns it until you pay them off. Mortgages have artificially inflated all property values due to them being available to every moron willing to buy something on a 30 year note with an obscene interest fee, all for instant gratification.

Owning property free and clear can be very rewarding. Treat the purchase just like you would with the other things mentioned in this list, cash up front, do not buy it on credit, and keep it simple. Paying rent is an expensive recurring cost with zero return in investment on the property IMO, except for maybe being able to walk away without much repercussions. You are also at the mercy of a landlord should he decide to do something with the property that is not to your liking. Rent is seemingly an expensive cost to have a temporary roof over your head.

If your goal is to save money and eventually own a place, then if you have no choice but to rent, do it small. You are paying for a shelter, not an extravagant night club to entertain guests. Again, K.I.S.S. principles.

It may seem daunting and could take years of saving up in order to accomplish a property purchase, however it can be done. One could always start small, buy an acreage somewhere, build a little cabin on it, move in and improve it over time or build another dwelling while living in the cabin. Or conversely pick up a fixer upper for a few thousand, fix it and live in it or turn it and use the profit to invest in your next purchase.

In the end you might have something to leave your next of kin, or even a place for them to build on while you are still alive. A mortgage just leaves a debt if you die before it’s paid off, renting is neutral and leaves nothing (which is fine), owning a place even if small leaves something however.

Aged 45 I live at home with my parents despite being worth over half a million dollars. Makes getting western women almost impossible, but I save a huge amount of money; money that allows me to work or not work as I please, and make occasional flights to the Philippines for sun, women, diving, and relaxation.

Get married, every study has shown one of the largest factors of long term financial stability is marriage, but good luck finding a spouse in this relationship market who won’t clean you out in divorce court. If you can make it stick with a woman you trust, it’s worth it.

You cannot trust any woman. There is always an incentive for her to take you to the cleaners.

There are simple steps to this.

Trusts – when you buy a house put it in a land trust when you buy it. Kids, set up trusts for them. So if the wife leaves you can dump part of your money into these so she can’t walk with it and this makes a safe location for portions of child support money.

Retirement/Banks accounts – never have anyone’s name on your retirement account beyond being a beneficiary to allow quick possession in the even of your death. You have a joint account and your own personal account, same goes for her. As mentioned above you only add names as beneficiaries. The bulk of your direct deposit goes into your private account and part into the joint for living expenses. Don’t play games with your money or accounts if a divorce is looming, judges do not like that.

Precious metals – buy silver coins/ingots whenever you have some spare money and put them in a safe that’s located in a trusted place. Junk copper and brass are also good but worth as much if you don’t have the storage room or time to collect. Platinum and Palladium are better large scale long term investments for stability.

Obviously a prenup should be first and foremost. That’s a different discussion.

Great advice.

Get married – with an airtight prenup.

I am glad I own my home

The question of whether own a home can’t really be addressed in one paragraph. I understand the sentiment of this article. But keep in mind that investing in real estate is one of the few ways to get rich. For most everybody reading this article, it’s either that or owning your own business that employs a number of employees.

I have gone the route of real estate and don’t regret it. But yes, it does tie me down to a certain extent. It’s also allowing me to retire (at least semi-retire) at 47 rather than in my 60s.

Yeah, I personally am with you but I think the homeownership question can go either way. It can be a good financial decision, but only if you put a good bit of money down and stay in the same house for a decade or more. Otherwise, I’d advise renting. And if you are young, rent, because you want to be free and flexible, and plus your income changes and in a year or two, you can likely afford a much nicer place. Very easy to “rent” up to a better apartment.

I have friends who get these 2% down mortgages, and they think they are homeowners, but they are really just “renting” from the bank, along with being responsible for taxes, insurance, and maintenance. When they sell they have little to no equity.

What’s the APR on that 2% down mortgage? Just saying they got a “2% mortgage” doesn’t make it an inherently bad thing – but yes, the most likely answer is that it is a bad thing.

The other option to consider is to buy and live in the home initially (this gets you best possible mortgage terms) then leave after a year and rent it out. I’m probably following the late-night infomercial get-quick-rich plan, but it’s working for me. Buy a home, get a max mortgage (just short of hitting PMI), live there a year, then rinse and repeat. If values are increasing, it’s possible to get a mortgage plus heloc for the full purchase price of the home, which effectively means you’ve got zero of your own dollars into it. That way you can put your money into another property. If things tank, I walk away and the bank repos. If values start falling, just stop buying. I’m not even doing this for the immediate month-to-month return, I’m doing this to have renters paying down the principal on the loans. 10 years from now I’ll just refinance the properties to get cash out of them via the refi. Nothing illegal or immoral about it, just leveraging compounding value plus the principal paydown.

If ROK ever wants a more in-depth article on doing this, I’ll be happy to contribute. I cashed out every penny of my 401k (and paid the penalties to do so) to go down this route. I don’t regret it. If housing values fall 10, 20, 0r 30%, I still won’t regret it.

I’m not even talking about the interest rate. Regardless of the interest rate, due to the way that loan balances decline, if you have a miniscule portion of equity and huge amount of debt on a property, your debt balance will barely decline in the first few periods. Look at a loan balance graph.

http://dsearls.org/courses/M120Concepts/ClassNotes/Finance/Loans2b.gif

The slope is almost horizontal at the beginning.

So if you only put down 2%, it’s so meaningless I don’t know why there is a down payment requirement at all. Here’s a scenario: $100,000 house, put 2% down, live in it for 5 years, sell it, assume it appreciates at 2% a year (this is really just inflation, and not a real *gain*), 5% interest rate, and you pay 6% sales commission:

Purchase: $2,000 down, $98,000 financed

Sell in 5 years for $110,400, less commissions of $6,600 or $103,800

Loan balance is $89,900. So you walk away with $103,800-89,900 or $13,900

In the meantime, you’ve paid $23,900 in interest to a bank. The bank earned the vast majority of the profits (implying you’d be better off in the lending business, as another poster here alluded to).

And this is as good as it’s ever gonna get. You’re LUCKY to get appreciation right now, many properties have remained flat for the past 5 years. You’re LUCKY to get subsidized below market interest rates. These numbers get WAY WAY worse if interest rates return to free market levels, which eventually they must. Also, if an A/C unit or roof needed replacing during that 5 year period, those profits could vanish quickly.

If you put down a good bit (I always recommend 20%) and stay for more than 5 years (or keep the house and rent it, although this probably violates the terms of your mortgage), then it can work, but the scenario you pointed out is not a model for a national housing plan.

Agreed on everything you’ve written and it’s something that people need to understand. What I am doing is in now way shape or form healthy for the housing market overall. It’s simply a case of looking at risk, reward, and what the other potential opportunities are for investment. Your purchase/sell scenario has to be compared to other options (i.e. renting) and what profits/losses are the result of each scenario.

Homeowner here, and can definitely tell you that homeownership is the best choice ever. If you’re spending 1/4-1/3 of your monthly after-tax income versus investing 1/4-1/3 of your monthly after-tax income, the choice is clear.

Do your research, don’t overpay. Know the area. Know “what’s up and coming”, etc.

#6 happens to be something I did very recently.

I canceled that expensive gym membership and now I have the gym at HOME. The only things I got: Bar Fix and Bench Press, among a few other equipments.

Not only does this save me money, but I’m also more motivated to workout daily. My #1 excuse was always: I’m too lazy to GO to the gym.

Well, now the gym is only 5 seconds away. 🙂

I see a lot of anti home purchasing advice these days. Renting may be the way to go for a lot of people, but there are some really good aspects to buying if you do it right.

I have friends who have done this on my advise and it worked well. This is a great plan if you are in your 20’s

1) Buy a 3/2 home for about $230,00 in a decent but improving area.

2) Buy it completely renovated or flipped so there is no deferred maintenance or big repair costs in the near future.

3) Your mortgage will be about $1300/mo

4) Your friends are paying $1100 – $2000/mo for 1 bed apartments in the same city

5) Rent one or two of the extra bedrooms out for $500/mo

6) Deduct your interest and prop taxes and get a bigger refund/ pay less taxes

7) Bought right, the property should appreciate on avg at least 3%/yr which is $6,900/yr at the start

8) You’ll also be paying off $3,600/yr in principal and that amount will increase every year

Your effective rent is $300/mo. Your equity increases by $10,000 plus per year and that amount increases every year.

You get about $11,000 in tax deductions. The standard deduction is $4000. That means you get $7000 in extra deductions. If you are in the 25% tax bracket ($37k – $90k) that means $1750 in saved taxes/increased refund.

If you want to travel for a bit, keep your place and still have your roommates pay most of your mortgage.

Lose your job? Well, where are you going to get a place for less than $300/mo anyways? Only paying $300/mo you should have been able to save a nice chuck of change for a rainy day like that. Worse case, move in with mom and rent your room / rent the whole house / sell the house.

If you don’t like the house or city anymore, you can sell it or rent it out and keep it as an investment. In my area a house like that would rent for $1600 – $1800/mo. That’s shooting for around break even cash flow once you factor in vacancy and management and repairs and maintenance. It still can be a good move to hold if the house is appreciating. Plus rents will go up over time if its the right area and eventually it will yield a positive cash flow. (Hold it till it’s paid off and you have a cash cow, plus if it appreciates 3%/year you’ll have a paid off $558k house in 30 years)

If you like the house and get too old for roommates, get rid of them and have the house all to yourself. You’ll still be paying less than your friends who are renting 1 bedroom apartments, especially as rents keep going up.

If done right, home ownership can give you a lot of flexibility and be a huge financial plus. If done wrong it can be a burden that sucks all your free cash / free time in maintenance / and can keep you from life goals like moving cities or travelling.

As far as buying right, that depends on the macro environment and what’s going on in your area. Is your area growing in jobs and population? If not, it may not be a good place to buy.

As far as trends – millennials are staying closer into and re-populating cities – stay away from suburbs especially those with lots of baby boomers and older. That age cohort will be selling to downsize and selling due to death faster that people will be wanting to buy in those areas.

As far as global Macro, we are heading into some really weird interest rate environments. Rates are at historic lows, but market structures are keeping them from raising because a rise would tank the world economy. If the whole world economy blows, you’re screwed whether you are renting or owning. If interest rates stay low or get even lower you’ll do well to own.

Well said. There are always areas were property bubbles occur, but most of the young today are not marrying or starting families as ealry, so they will need less space. After seeing what happened in 2008 I was wary of investing in the markets.. the adjustment thats coming is going to be catastrophic… and bought property. Like you said, the location needs to be near an area of econmic growth if you are looking to maintain or increase value, but I simply like the security that it’s mine no matter what Comes. I could stay, rent or sell at my leisure.

Couldn’t agree more with this. Amazing analysis. Most important thing is to do your research on the area, or talk to someone who knows.

I know it’s not the most hardcore exercise out there, but walking around the neighborhood is still a decent way to stay decently fit. Way cheaper than the gym anyways.

Anyone here succeeded in creating a passive income? Im about to be debt free very soon and started thinking of becoming financially free. Dont know how yet, but thats my goal.

I’ve been playing with the idea of creating a chain of CD’s that are reinvested after they mature and loop the cycle to the point where I have 1+ maturing every week, but the interest rates are so low that it’s not worth the time and effort.

Ha, pre-recession, it was as much as 5%, I remember.

Yeah, now the best rates that my bank offers is 0.75%. I thought it was a joke…who would tie up a grand for an entire year just to get a couple bucks in interest?

You’re better off just buying a solid stock that pay dividends. You can get 3% or more depending on the stock. Plus you get the price appreciation if it grows. They could also increase dividend payout. I owned Phillip Morris back in the day and it has branched, spun off othet divisions and so on. It was my best stock and still have all the new companies they spun off.

Dividends are taxed at 15% Federal so it’s much less than income. No FICA taxes either.

That right there is why government mandated interest rates are bullshit, and can only exist with the federal reserve printing up excess dollars and passing them out to its member banks. NO ONE would choose to risk their capital by loaning $1,000 (that’s what a bank account is, even when it’s a guaranteed savings account, the bank is taking your money and loaning it to others) for $10 at the end of a year. That’s absurd, and real interest rates would be higher if it was based on simple supply and demand.

I haven’t used it myself, but peer to peer lending sites like Lending Club and Prosper offer the potential for decent returns. Yes, you are an unsecured lender, but I’d imagine if you stick to those with sparkling credit, and allocated your money over enough notes, you should do okay.

I was thinking to save as much as I can over the period of 4-5 years, and then open a hotel/hostel in Latin America where my GF is from and cater to international tourists.

You might want to check the profit margin on those hostels already in that industry and find out where the ROI is before making all the effort. The time and money you spend might make the break-even point too long to be optimal.

I will definitely measure all the pros and cons. This is just an idea for now. What I know is that there are hundreds of thousands of Westerners traveling to Latin America. And oftentimes the service quality they receive is quite bad. Sometimes people dont even speak comprehensible English.

It’s weird, as someone’s who traveled to hostels domestic and abroad, I’ve been to ones in English-speaking areas where the employees spoke poor English (Miami Beach, Vegas), and ones in French-speaking areas (Montreal) where the employees spoke excellent English.

What were your main complaints about hostels abroad?

Primarily in Australia, 10-12 people to a room, one bathroom per floor, and the front desk staff weren’t the friendliest. Also, stolen food from the pantry and overcharging for booze, but I suspect the latter is normal.

I’ve pondered on a similar idea…basically purchasing 10-15 acres of land and building smaller homes to rent on them. There’s some blueprints for 300-500 sq ft houses, perfect for an individual or minimalist and it would cost next to nothing to build those houses.

Thanks

Would you do it in the US?

Yes but it’d have to be in the right market.

I could see that working, I think hipsters would be all over it. And they are the target market for housing because they are just graduating / moving out of the parents and all need a place to live. Right now there is a hipster focused retail development that is built on shipping containers with holes cut into them for windows and doors. Costs almost nothing to create it, but the hipsters are going crazy over the idea. If you built cheap, tiny housing near a development like this it would sell out fast.

I suspect you’d be better off with an Equity Index Fund that traditionally brings back around a 7% rate of return on average (since the late 1920’s actually). That’s starter level stuff, but it is a good place to start, but don’t just stop with that (a lot of people do). I also recommend looking into Edelman finance folks (Ric Edelman). I get nothing from that, just somebody that I’ve had great success with with my finance. Avoid day trading like the plague, at least for a couple of years until you really know how things work too (in fact, I avoid it entirely now).

I’ve done so with real estate, but it’s a joke to call it “passive” … its a LOT of work.

Mainly because of shitty tenants?

It basically comes down to (1) shitty tenants and (2) the if-you-want-something-right-do-it-yourself adage.

Shitty tenants are a nightmare. And the laws are in *their* favor, not the landlords. Basically, the laws were written for an Andy Griffith era, where, imagine a young guy goes off to visit a sick aunt, stays to take care of her and can’t return home to make the rent payment, the law protects him so he won’t come back to an apartment where the locks are changed and his stuff is thrown out on the street, basically he will pay a penalty / fee and keep going.

But if you have a deadbeat who refuses to pay you, ignores your phone calls, and gets a month behind, you can’t do anything yourself about the situation. You may think you own the property, but you are not allowed to go in, cannot change the locks, can’t remove them, but must instead use the court system, which costs *YOU* approximately 1 months rent in legal fees and court costs, and can take from 2 to 6 months. Bad tenants know this, so move in, pay a couple months, and then live rent free for the remaining 6.

What has really hurt is the poor education system and declining culture. I can only imagine the quality of tenants will drop substantially over the next 20 years, as people no longer have common decency, courtesy, honesty, etc. I’ve cleaned up dirty diapers and bags of garbage and clothing that were left in abandoned units.

The other point is if you don’t do EVERYTHING yourself (well, I hire out a plumber and roofer sometimes), you will get screwed. Managers and maintenance companies take advantage of you. They are lazy and have no work ethic. They do shoddy work, overcharge, or fix things that weren’t broken and then bill you. I’ve used half a dozen management companies and hired individuals and it’s all the same. Basically the culture and morality of this country are broken, and the system relies on a basic level of honesty and good nature in order for things to work. I’m about to take a 6 figure loss on one deal. But the ironic thing is, the tax laws are written so strongly to favor real estate, that it will be mostly offset by the same amount of tax savings in the years I’ve owned it.

If you are going to personally screen tenants, show your vacant unit, come over every time they call with a problem, and do all maintenance, then I say go for it. But if you log your hours you will find it’s not a very good return for your effort.

I knew being a landlord is pain. In Quebec Canada, for example, damage deposits are against the law. I saw people trashing places beyond any limits. You’re right, as a landlord you dont have many rights. An idea that I have is opening a hostel in Latin America catering to Western backpackers mainly. I know what they want and my GF is from there.

I see a lot of foreigners doing that sort of thing in Latin American countries. Some even get by in places as small as a 4 room B&B that rents for $30 a night. The cost of living is so low, they don’t need much to live off of, and the stress involved with only 4 rooms is pretty low. Basically just cook a kick ass dinner every night and chat it up with some strangers.

I recently tried to stay in an awesome B&B in Latin America for $30 ran by a European couple but it was all booked up. Plus foreign travelers, as a whole, aren’t gonna wreck your place, maybe steal your towels at worst.

I’d stay away from rental properties. As a CPA, I’ve seen few people do well enough with them to justify the headaches. I’d hardly consider it “passive” income, unless you hire a property manager, which will cut substantially into your profits. Most of my clients bemoan the difficulty in finding good tenants, and one who trashes the place can wipe out years of profits.

I became debt free last year-house, auto, credit cards & student loans-all gone. At 41, I have lots of time ahead of me so I’m looking into passive income sources as well. Not a big fan of the stock market (too volatile for me) but I’d definitely avoid speculative strategies like day trading and even individual stocks. Few people do well with them.

I’m considering getting into lending. I’ll have little trouble getting 8-10% returns or more with modest risk among the pool of people I’m looking to deal with.

Good advice. I’ve made 2 real estate investments, one small one that has turned out great, one big one that is an ENORMOUS disaster. The bad thing is, there really IS no good place to invest these days. It literally is a “war on savers” I don’t know what to recommend, after one becomes debt free. I do invest in energy stocks, because no matter what, people are always buying energy.

Sorry to hear about the real estate debacle, something I’ve seen my fair share of among my client base, unfortunately.

Another thing to keep in mind is that rental real-estate losses, capped at $25,000/year (unless you qualify as a real-estate professional), start phasing out after $100,000 of AGI if filing a joint return. They roll over and can be claimed in full upon disposition of the property, but may not yield an immediate tax saving.

I agree, there is nothing out there that is a “slam dunk” as far as investments go. I’m not a financial adviser, but clients ask me my thoughts all the time and there just isn’t much good news to give.

I think real estate is generally over-valued at the moment, interest rates are piddling, and more mature clients closing in on retirement don’t want to deal with the stock market roller coaster…

The best thing real estate has going for it is a long list of government subsidies and incentives that make it a better bargain than it otherwise would be: (1) deduction of operating expenses (and I’m sure this one is abused heavily–who is to say whether you are using that new lawn mower only at your rental property or also at home, or where those cans of paint actually went?), (2)mortgage interest deduction, so you can subsidize your purchase of the property itself, and (3) depreciation (an odd IRS-only calculation where you assume your property *declines* in value every year, when typically the opposite is true). Then any profit you earn can be transferred tax-free to another investment (1031 exchange). Finally, the use of (5) leverage makes it unique. One can use $20,000 to buy a $100,000 investment, and if it gains 5% ($5,000), that is a 20% gain for you ($5,000 return on $20,000). It’s hard to argue against real estate with these 5 big advantages in its court. Take them away, and there are much better alternatives.

1031 exchanges are a great way to dodge the tax man that surprisingly aren’t used as much as they should be. Also, converting a rental to your primary residence for at least two years will allow you to exclude any gains as well.

You’re an accountant, right? What area geographically do you work in? I’m in SE USA.

Yes, I’m a CPA. I’m in the Buffalo/Niagara region of upstate NY. I have a condo in Ft Lauderdale as well and try to get down there as much as I can.

Yes, I’m a CPA. I’m in the Buffalo/Niagara region of upstate NY. I do have a condo in Ft. Lauderdale as well, try to get down there as much as possible.

I do some estate valuation work for CPAs sometimes. Licensed in 12 states, from Virginia to California. Nothing further north though. Let me know if we could ever work together on something. I’ve always wanted to see Niagara Falls.. last girlfriend shot down the idea every time I brought up taking her there on a nice trip where I would have paid for everything.. haha.

That sounds good!

As for coming up to Niagara Falls, worth the visit, but not enough to do to spend more than a few days. Hopefully you have a passport or enhanced driver’s license. I’d check out Niagara on the Lake, Ontario and Toronto as well. Also, Buffalo is only about a half hour south. Let me know if you come up!

One other thing that might be viable, but I have limited knowledge of, is operating a trailer park. All you provide is the land and utility hookups. The lot renter provides and maintains their own trailer. They have an incentive to keep current with the rent since eviction means they incur the cost of moving their trailer. Obviously amenities offered will be minimal-people don’t expect on-site fitness centers and such.

Do you have a spare room or garage you can rent out? I live alone and my property has a double carport and lockup garage. I rent out the garage to a guy you owns a vintage car so he uses it to store it as he doesn’t have the room at his place. I also rent out one half of the double carport to a guy to store his car when we works away at a mine site two out of every three weeks. It’s cheaper for him than airport parking.

So for the garage I get $40/week and for the carport I get around $1000/year so a total of $3080/year AUD for just letting a couple of cars sit there.

Overall good article. I disagree with the renting over owning, though. Where I live in upstate NY, housing is very inexpensive. Get a home around 1,000-1,500 square feet, and your utility bills will be low, maintenance will be easy and taxes won’t be too bad.

Also, gym memberships are generally inexpensive these days. I agree with others that, eventually, you will want to move beyond body weight exercises.

Getting involved with the wrong women is, IMO, the #1 surefire way to destroy your finances.

Great advice overall, although I’m not entirely in line with everything.

Buy the best *quality* you can get for the money, as opposed to the cheapest or simplest. I buy a very nice car once every decade….BUT…it’s top shelf quality, I pay a bit more for it up front, and then drive it until there’s nothing left but duct tape and transmission fluid. The plan works like this:

1. Buy car, pay if off as fast as you can. Put as much down on it as you can afford without harming your investments otherwise. If you’re on payments, pay above the monthly payment towards principal.

2. When you’re through paying it off, continue to make the same “payment” to a set aside bank account (or if you’re like me, put the money in your huge fireproof gun safe).

3. Drive until it’s rust, bondo and needs to be towed out of your driveway.

4. Then walk into a dealership and buy a new, high quality nice car with the money you were paying yourself (step 2), cash on the barrel head.

5. See step 2, only this time, you start with zero loan to pay off.

6. Lather, rinse, repeat

Just bought a car not too long ago, paid cash up front, had the title sent to my house, badda bing, no debt, new car, and off we go.

Something else: WTF is with shampoo hate? What is used in its stead?

To add to point 1, after you put down as much as you can and if you can swing it, open a Chase credit card with only 2% balance transfer fee, 0% APR for 12 mths. and pay the balance principle with that. Divide the payments into 12 equal months so you don’t incur interest. Don’t use that card at all for any purchase.

Benefit is (1) you only pay 2% for the loan instead of 5% for years. (2) If you’re tight on funds one month, you can pay less and it’s ok. Just pay more the following months. And (3) you get the title because it is an unsecured loan. You lose your job and can’t make the credit card payments, they can’t repo the car.

If you can find 0% balance transfer fee, jump on it.

Edit: Key is you must pay it all off before interest accrue.

I have a 15 year old Toyota Tacoma with over 220,000 miles. It has never had a mechanical malfunction. I am rough with it, too. I carry trash and stone and all kinds of crap. I will drive it till the wheels come off.

17 year Toyota Tacoma. took it in for a shop to repair anything they could find. replace the light on the license plate, that’s it.

God bless the Toyotas. It’s damn hard to kill any of them even if you’re a complete fuckhead mechanically.

1996 Subaru stationwagon, built like a brick shitehouse.

Great advice on the car. Regarding the shampoo-hate: I think it likely has to do with the fact that no man alive used it until a couple decades ago, and most guys’ hair does just fine with water rinsing. Water washes off sweat and dust just like it always has. Anything more potent/toxic/sticky can be dealt with by normal soap, no need for another product.

Disagree with getting rid of gym. If you can find a good full utility gym (not planet fitness) for $50 a month or less it’s more than worth the money if you actually use it. One time I wanted to save money and toughen up for real and just lived out of my car for 3 months using my $15 a month gym for hygene/kicking back in addition to everything else rather than extending my lease. That was roughly $5000 saved on rent and utilities and $45 worth of gym fees made it possible.

I actually know several people who did the same thing. Slept in the bed of their pickup truck with a camper shell or in the back of a cargo van, and used their gym memberships to shower/shave. Did it long enough to come up with the cash for a down payment for a house.

I want to save a wad of cash and then once I can go semi off the grid, take to the road in an RV and boondock. The added benefit is if Idecide I want a plot of land away from it all to ride out the Zombie Apocalypse…I just drive in and pull up stakes.

17. Don’t waste money on Apple products.

I’m not an Apple guy, but their hardware does seem to be reliable. I have an ipod touch I bought 4 years ago and other than shattering the screen a few months back, and declining battery life, it does everything I need it to. I bought an ipad and it is handy, fun to browse ROK and a couple of my favorite sites before going to bed, and the battery lasts well over a week. I think some of the cheaper alternatives don’t hold up so well in the long run. As for computers, I am pc all the way, build my own machines. I’m on a 5 year old desktop now, the only thing it needs is an upgrade to SSD drive.

I never said the hardware was not ok. It is simply overpriced, especially when it comes to prices of the previous generation of devices. You can save a lot of money by buying e.g. a Samsung mobile phone that came out 1 or 2 years ago. If you do that with an Apple phone, it will still probably cost 2/3 of the original price.

Nothing personal, but let’s all try to cut out the “I never said” quotes.. I know you didn’t say that, I’m simply expressing an opinion about hardware quality. And if I DID think you said something which you didn’t, then your position was unclear, so clarify it. Sorry, just a pet peave I see online all the time. No one cares what a stranger did or didn’t say in a past anonymous comment, just make the point for the other 99.9999% of the readers besides me 🙂 OK rant off.

As for the phones, yeah personally I use a flip phone, and think it’s insane to spend $500-$900 for a telephone (I have a $60 Nokia plus a $500 ipad). Total cost is less than what most people spend every 2 years on Apple or Samsung stuff, and I don’t plan on replacing either any time soon. What really gets you on these smartphones is the service plans. I pay $20 a month, including taxes, for unlimited talk/text and it even gives me a smidge of data if I ever needed that in an emergency.

No one cares about your anonymous pet peeves either

Blackberry Curve + 32gb expandable memory = godtier MP3 player, all for under 100$CAD. Been going strong for 7 years with it.

I bought a Nokia lumia 920 a few years ago and it’s been a reliable phone and

you don’t have to put up with the intrusive apps like with Android phones that

need permission to access your information.

In regards to saving money on alcohol, I’ve found that the best way to accomplish this is never purchasing alcohol when eating out, just at the grocery store, and always going for the big bulks (like 12/24 packs) when buying it. In my area, a single can of Pabst costs something like 70 cents if purchased as part of a 12-pack, but at your average restaurant you can expect to pay $3-4 on average for a Pabst.

Car – can’t speak for this one enough. I got talked into buying an expensive ass car, by an older man who is far more established (who also has a wife with income), and I can’t tell you how much I regret that. My entire monthly savings and leisure money is now going into that and I can’t tell you how stressful it is. Only thing on my mind now is “work harder, get promotion, make more money, to get out of this self-inflicted debt.” Chalk it up to a lesson learned. I will never play the new car game again. Nope! Find me an old beater or something reliable for $1500-1800 and let it rust out before I get a new one. My dad had the right idea. I should have listened.