As late as 1970, almost half of all jobs had a pension—a guaranteed income you would receive upon retiring after working a certain number of years in your field. Combined with social security income, which is generally enough to provide basic housing and food needs, a man could retire quite comfortably, and without ever needing to know anything about investing. Times have changed, but I’m going to show you how, if you start early enough, you can become a millionaire by the age of retirement, even if you work at McDonalds.

Start Young

When I entered high school, my father took me to the library, introduced me to some books on finance and investing, and a service our library had called Value Line, a series of large books published by an investment research firm which reported data on thousands of companies and mutual funds. Being good in math, and interested in statistics (particularly books on gambling and statistics—side note: blackjack is typically the best game to play at a casino—roulette is among the worst), I was fascinated with the idea that one could save their money, and it would grow in value.

The Power Of Compound Interest

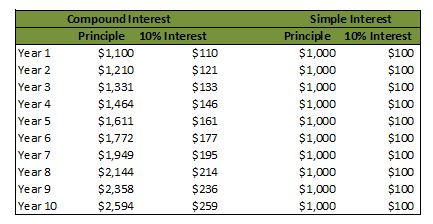

Compound Interest is the repeated effect of earning interest, and then adding that interest to your savings, thereby earning a greater amount of interest the following year. As an example, imagine I loan you $1,000 at a 10% rate of interest. In a year you must return $1,000 principle plus $100 in interest to me, leaving me with $1,100. That is simple interest. But imagine I then invest my $1,100 in a retirement account that earns 10% each year. By the end of a decade, instead of $100, I will now be receiving $259 in interest. This is off the same $1,000 investment I started with.

In order for someone to earn as much as me in year 10, they would need almost $2,600 in savings, while I invested only $1,000, and that was a decade ago. I never added another penny of my own money to my account, and already you would need almost 3 times as much money in savings just to keep up with me.

The effects of compound interest are exponential, and as time increases, the end result of savings increases more rapidly with every year. If you remember no other concept, remember this. The longer the time period, the greater the money.

When I was 15 I began working at the local grocery store. I worked 5 hours a day after school, plus weekends, earning a bit less than $250 a week. Now, a 15-year-old has little need for thousands of dollars, so I saved the majority of this money. That year, I opened a retirement account with $2,000 (less than 10 weeks of work, which was easy), and still had plenty left over to spend.

Retirement Accounts

IRA is gonna get you some money

You can use the basic concept of compound interest to make you money. But there are some extra things you can do to increase your returns even more. Most governments encourage saving for retirement, often with subsidized or tax-advantaged retirement accounts. The US Government offers Individual Retirement Accounts, which allow money to grow tax free. I recommend a specific type called a “Roth IRA” which we will discuss here.

Live Frugally

If one lives frugally, it is easy to save enough to fund a sizable retirement account. I had a great professor who told me that the year after you graduate college, you will make more money than you have ever seen in your life. Perhaps you have a part time job earning $5,000 or $10,000, and you currently live on a fraction of that. But next year, you will be likely earning $30,000 or more. Most of you will spend $30,000, or close to it. But you could also choose to live off $10,000 as you have been doing, postpone making your big purchase of a car or whatever for just ONE year, and save as much of your income as you can.

If one lives frugally enough, one can easily save enough to fund a retirement account, even off minimum wage income. This is an extreme example, as practically no one works for minimum wage for more than a couple of years at the beginning of their career, but it goes to prove a point: there is NO excuse for not being wealthy later in life. Today someone earning minimum wage at 40 hours a week earns just over $15,000 a year. By saving 20% (only $60 of each $300 paycheck, or roughly an 1 hour a day), one can invest $3,000 in a retirement account.

Saving 20% of your income is not easy, but it IS possible. If one starts at age 20, and earns the historical rate of return of 8% in the stock market, how much money will one have at age 65? Take a guess. The answer: $1,159,517. Think about that the next time you look at a McDonalds employee.

But most of us already earn well over minimum wage. What happens if you invest the maximum allowed every year into your IRA (currently $5,500, and increases over time)? With the same 8% return, you end up with over $2.1 million at age 65. If you really don’t know how to live frugally, pick up a book on the subject. It’s quite easy to find extra money by cutting out bad habits.

Long Term Low Cost Investing Through Index Funds

When I first started investing, I bought the stock of the company I worked for (bad idea—they later went bankrupt leaving me nothing). I then tried mutual funds, which did better, but I was paying exorbitant amounts in management fees to Wall Street Managers who were not performing any better than other options. The answer many have turned to today is Index Funds, and the champion of this is John Vogle of Vanguard Funds, one of the largest investment firms in the world.

For over four decades, Vogle has been pushing the idea of getting Wall Street out of the equation, doing no trading, and simply owning a basket of American businesses by investing in an Index Fund (a group of hundreds of businesses). As Vogle puts it, “then you are creature of the market, not of a casino.”

These funds are much cheaper, because there is no active manager; they simply perform as the overall economy, or a defined sector of businesses, performs. The performance of these indexes as a whole is actually BETTER than managed mutual funds. One of the most popular funds in the world is the Vanguard Index 500, which mirrors the S&P 500 that is a mix of 500 of the largest and strongest companies in America. If you invest in this, when the news reports “The S&P Index was up 2% this month” they are talking about your return.

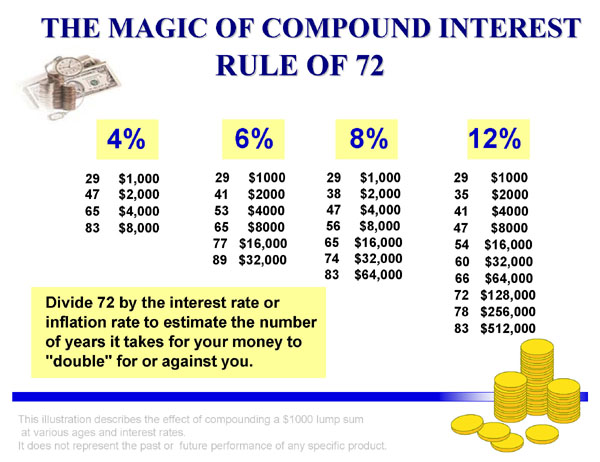

The Rule of 72

While there are many online calculators that can calculate projected returns for you, a simple way of gauging performance is by using the “Rule of 72.” It’s very simple. The rule tells you how long it will take for your money to double when invested at a compound rate. Simply divide 72 by the interest rate. The answer is the number of years for your money to double. 72 / 10% = 7.2 years. 72 / 5% = 14.4 years.

Risks

Unfortunately, this system doesn’t work nearly as well as it used to in the past, and we are in for more financial turmoil and changing of the way investing works in the years to come. Here are some risks:

- Risk of loss: Your investments can lose money.

- Risk of reduced returns: Stock investments in the past averaged around 8% returns in the long run. If this does not hold true in the future, your returns will also vary.

- Risk of Inflation: Inflation destroys the purchasing power of your dollars. While a million dollars today would be a comfortable amount to retire on in many areas, by the time you are 65, a million dollars will buy far less than it does today.

- Risk of Government Regulation: Governments may renege on their agreements to leave retirement accounts free of taxation. Since most people do not adequately save for retirement, the masses will be in favor of taxing your retirement funds

- Risk of Playing Catchup: If you don’t start early enough, you must save FAR more to end up with the same amount as someone who started just a couple of years before you.

- Opportunity Cost: If you are saving 10% of your income, you have 10% less income to buy the things you want today. You could get hit by a truck at age 64 and all the years of postponing gratification would be for naught.

Even with all these risks, you will be better off if you find a way to save for retirement, than if you don’t. Get ahead of the game, and give yourself financial freedom in the future.

In summary, if you are not saving for your retirement, you should start today. Educate yourself, make your own decisions, and don’t rely on any one source, including my advice here. Set up a monthly auto-pay where money is deducted every month into your retirement account, and get on the path to a stable financial future.

Nothing is guaranteed, but saving now will put you miles ahead of most others. One final bonus—retirement funds are excluded from many sizeable assets. They aren’t counted towards college tuition funds, and they can’t be taken by most creditors.

Read More: Expensive Woman Seeks Retarded Millionaire

Great article, if you write a follow up then address covered call writing. One of the best finance books Ive read is Option to Profit

A reason to get out of debt.

But stocks 8% is a dangerous myth. There were zero gains between 1966 and 1982 along with inflation.

You are likely to have no job at the bottom and might need to sell at the bottom.

Japan peaked in 1989 and has not topped 39000 since.

1982: perfectly safe 30 year treasuries paid 16%.

1929 took till 1953 to be exceeded.

Cypress was bailed-in – they just went in and raided the accounts.

They can change the IRA laws any time.

Bank accounts used to pay 4% before we went into speculation, but it was constant. There was little debt.

Now companies have loaded up with debt and have been buying back shares. When the debt pyramid collapses (2007-9) the companies may go bankrupt and your stock goes to zero. People hate stocks at the bottom, but if you have cash, you can buy the viable survivors.

Invest in yourself, not college but useful skills. Construction, electrician, plumber, mechanic, maker. Math and science and engineering. And your health and body.

Incorrect. If you had a diversified global portfolio with 60% equity and 40% fixed income, you would be out ahead even counting the 08 recession.

Unfortunately no one has a time machine. Even the author wasn’t suggesting a diversified GLOBAL portfolio. And is ahead 8%? And if you don’t sell now or churn, will you still have those same returns two years from today (I expect a top, then a relentless drop, maybe a crash, but like 4/31 to the bottom in 32 – no crash, just losing a few percent each month on average – and those compound since going 100 to 50 is a 50% loss, but 50 to 100 requires a 100% gain).

So if you cherry pick methods, sectors, or managers, you can always find a few that beat the average but not because of any inherent correctness, but luck. Amazon is now worth more than Buffet’s Berkshire. Blackberry is hanging by a thread, Apple is receding, Alphabet/Google is questionable. China is going into recession as is Brazil. The EU and Japan are stagnant and have been . VW has been found cheating and may be bankrupt. Could you predict any of this 10 years ago – 2006?

For some historical perspective, read Robert Prechter’s “Conquer the Crash”. Everyone was saying Inflation!, but we got deflation which he and a handful of others predicted.

There was the South Seas bubble in England and the Mississippi scheme in France, and the Tulip Mania in Holland. Condemned to repeat…

I agree with the general point. We need to diversify. One hundred percent in stocks is for people with a 25+ year time horizon.

100% stocks when they are at low to moderate P/Es. Investing at SPX 700 was smart, not so much at 2100. Just like “Real estate will never go down and if it does it will come back”.

Very few have that ratio

Most are net down since 08

Get your shine box now Tommy

Unfortunately, TPTB make that course of action not as viable as it once was.

For the blue-collar stuff, you’ll have to “compete” with illegals (and H-2B quasi-illegals) & unions (or, worse, have to join a union)

For the white-collar stuff, you need a college degree for most anyone to even consider you, despite your skill, and you have to compete with a literally unlimited influx of H-1B visa vampires. Even if you land a job in the field, those modern-day indentured servants have depressed the wages.

I have no High School diploma or GED but have been doing Computers, IT, electronics and everything between for 30 years. It is hard to get in to the traditional track, but those same dinosaurs are dying out. Locally, I could get any trade jobs – homes and businesses need things like carpet installers and carpenters. And there is the entrepreneurial track.

I have no high school or such diploma either, but I’m working as a Sr. Software Developer since quite a long time, but before that I did everything from shoveling horse shit to running a newspaper stand and answering phones in 6-7 languages lol.

Times have changed in 30 years and not for the better.

Now folks entering the industry need a BS degree just to get their foot in the door, irrespective of skill.

Trade jobs free of illegal competition and union/legislative interference? You must be in some right-wing paradise second only to Galt’s Gulch 😉

Employers are increasingly abandoning Haji and Ravi. Communication issues and poor coding are starting to bite corporations in the ass, hard. I can put out a resume at 8am and have two interviews lined up by Noon in this field.

Who knows for how long, though. You know how government always pushes for more skilled labour. They might just oversaturate the market and ruin it sooner or later.

On the other hand, from having been a programming teacher, I must say that simply not everybody actually has it in them – so much for equality. Maybe it’s an IQ thing, maybe it’s a personality thing, but many people are just rule followers and can’t bring up the amount of creative thought necessary to tell the friggin machine what to do.

By the way, do you know your MBTI type?

Maybe your field is miraculously exempt from the H-1B plague.

Even if it isn’t, I’d wager that the wages are still depressed massively by the H-1Bers.

I’d love for companies to abandon the practice of bringing in scads of undereducated, underskilled H-1Bers (and using American grads as “pump ‘n dump” tutors for ’em). But if they are abandoning it, why are the Feds letting even more in?

Under Dubya the H-1Bs were made limitless through loopholes and Lyin’ Ryan is bent on making it flat-out limitless.

On a teaching programming side note, I’ve noticed that my state school system encourages students who have little interest and aptitude into entering into comp sci.

Aggressive advertisement of their CS programs followed by 2 years of coddling and hand-holding with elementary Python and rudimentary Java with a dash of database. Then junior year hits and they drop advanced data structures, C and calculus-heavy “weed out” courses on ’em.

Even students who like and have aptitude in comp sci can be sent reeling by that sucker punch.

If it were a conspiracy to turn many a dream of a 4 year Comp Sci BS into a 6 year plan that results in a degree in a different field, it wouldn’t surprise me.

Advanced data structures, C and calculus-heavy? Sounds like a wet dream come true! But yeah, obviously not to the types of people you mentioned. That’s exactly what I meant. People think too much about “what is well paid and respected” and too little about “what am I actually good at?”

Nothing miraculous about it. H-1B’s are notoriously horrible programmers, and their ability to communicate is almost non-existent. The manager I work for now has openly told me behind closed doors that he’s never hiring an H-1B again for these very reasons.

There could be some merit to it all, if the harder courses weren’t so obviously designed as weed-out courses.

Who needs a course consisting of proving that some theoretical routine will run within certain arbitrary constraints, and why is it in the curriculum while topics relevant today-like multithreading applications or GPGPU-are not?

If we were talking embedded applications, and were in the mid 00s, maybe proving that your (simple) application could run in a few KB of memory would have a purpose but it is almost as outdated as the data forensics/cybersecurity classes that still focus on analyzing floppies.

I’m glad to hear that the “tide is turning” but H-1Bs are still here in force.

The bean counters and out-of-touch management are still high on the notion of hiring indentured servants who, while incompetent, are willing to work for peanuts and cannot “jump ship” to another company. 🙁

I’d still love it, though. I want to understand the basics before moving on to the more complicated stuff.

How long? I don’t care. I’m about to convert my farmland into hop growing land. My days of giving a shit about corporate America are drawing to a very rapid close.

Whats brewing?

Until corporate HR refuses to approve a salary high enough for anyone other than an H1-B to take the job.

They’ve been whining about the lack of american kids going into engineering and related fields for 30 years or more but the one thing needed to attract them they don’t do, pay on par to the productivity is. Instead they bring in foreigners to drive the wages down.

If I just got maybe 2-4% of the money I’ve made employers I’d be a millionaire. But if I don’t like the salary they’ll just replace me with someone from Pakistan or China or wherever who work for less than me. The corporate system considers people fungible human resources. They’ll have a body in the job and they don’t care so long as assignments get done. That above and beyond crap they tell us is the route to success just says you’re sucker willing to be worked to death. That lesson basically had to be beaten into me over about 15 years before it took hold.

Cascade or Mosaic hops. Or don’t you like IPA beers?

Those two together are what I look for hehe, a few USA based makers are doing incredibly good beer.

Left Coast Brewing Co. Has Hop Juice, very good, out of San Clemente CA. I could list many others but this is so far the King of them.

Good programmers are born not made. I would know as I consider myself a terrible programmer despite the fact I’ve been self-teaching C/C++, DirectX 9 & 11, win32 gui and a bit of web technology (php, ajax etc) I’m so jealous of programmers who almost seem to speak C++ as a first language. Templates are a notch above my abilities.

I strongly believe that a strong deflationary force in programming is open source. When you really think of it almost every quality product can now be had for free. As a consumer I benefit but as a wannabe programmer I don’t. Where is the time when a simple shareware published on a CD given out to a computer magazine would allow you to make money?

How about being granted a Nintendo seal of quality and sell SNES cartridges at €100 (not sure what Nintendo’s cut was though) And then there’s the whole app business too where you have to use the freemium model because nobody pays 99 cts for an app that another made for free.

I am in the world of physical things not software so such volunteer work doesn’t apply to my area and the same conditions exist.

Working for a union has virtually no downside. It is Collective bargaining and has excellent benefits. I don’t begrudge any Union guy. Especially in the trades.

Unfortunately, the opposite is true.

Working for a union has virtually no upside.

1.) You’re forced to support liberal politicians who actively work to destroy your employment and way of life.

2.) You’re compelled to follow the far-reaching rules of the union, you’re not your own man.

3.) You’re mandated to literally extort your employer, perpetuating a Marxist “class warfare” idea.

Unions are legalized-by the SCOTUS-socialist crime syndicates who work by extorting employers and whose leadership does not have the best interest of both its “rank and file” & its extortees-employers-in mind; when times are lean for you or your employer, the union brass ensures that they’re kept living high on the hog.

Unions ushered in liberalism and globalism, the two banes of our time.

nice post. around 1980, there were about 100 or so companies with AAA credit ratings. By 2008, it was down to 3.

No one ever talks about the stock buybacks- at some point, most companies will buy all the shares back and go private (thanks for playing at The Stock Market Casino! enjoy the voucher we left on the endtable! Good for a free weekend if used by Dec 31)

Don’t know that I’d say its a myth but definitely need to diversify as returns can stay down for long periods of time. Question is where? Bonds yields nothing – less than the S&P 500 does. MM and CDs yield nothing. Real estate and alternative investments about all that’s left.

Companies have debt but its long dates, very cheap, and leverage is actually pretty good. Extremely unlikely you see a lot of bankruptcies, even in a another 2008-2009 scenario – balance sheets are in *much* better shape now between longer dated securities, lower debt cost and much higher cash balance sheets compared to 2007-2009. For example, in 2007-09, hotel companies were levered around 7-9x and maturities were 2-3 years. Today, they are levered around 3-4x on average and maturities are around 5-8 years (and rates are lower) plus more cash on the balance sheet.

I’d argue invest in both yourself and college useful skills. If you want to make your own business be successful as a plummer, etc, helps to have a general business sense. Stay invested in stocks (25-50%) and also alternatives such as rentals and other businesses (25-50%)

Keep cash, perhaps gold and silver until things resolve. Then financial repression may not be obvious bet read the Austrians on interest rates and time preference.

I’ve got ~10% in gold/silver or gold/silver ETFs at the moment. Not willing to commit more to anything that yields zero and only grows in value on inflation or governments collapsing. I’d rather own rentals that also grow with inflation, tend to do better in recessions, and yield 7-10% today.

Goldbuggery is the dumbest thing in the world. You might as well collect comic books, which at least have value to neckbeards. What the hell good is the piss metal for besides deluding other Austrian Economics nerds into reading their lies?

My god, have you LOOKED at the price of gold over the past 10 years?

Sure have. I went up to about 20% of net worth when gold was below 800 and silver was sub $10/oz and sold it all in 2011. Up about 30% on my silver/gold investments this time. Gold looks great over a 10 year period. 5 year? Not so much. Diversity of investments and not staying “married” to one bet is a beautiful thing.

Only six thousand years of being recognized as a store of value. Jews with Gold could get into Switzerland.

Silver is the better exchange metal as it has less value per ounce to buy necessities.

But food will be even better when nothing is available.

Just look at Venezuela and ask yourself what you would like to have invested in.

Negative interest rates mean zero yields are better.

Rentals need maintenance, have property taxes, and hope you get good tenants that won’t burn down the property if you try to evict them for not paying rent. It depends on the area and the renter. Locally I would fairly trust things. Other locales make eviction nearly impossible, demand “fair housing” so you may end up with a Meth Lab, or something else.

You do understand what a cap rate/yield is, right? It’s the net of all expenses including a capex reserve and includes an expected vacancy rate. I don’t rent to people doing meth. It’s pretty obvious when you interview people who is legit and who isn’t. Here is a bit of advice if you get a rental unit: People who want 2+ years, are far more stable than those who want 3-6 months. Require 2-3 months upfront with 2 year lease, 720+ credit score and stable work history and your odds of issues is very low. And yes, I rent in areas that are “owner friendly” rather than “tenant friendly”

True, but the rental stands empty for months waiting for the 2+ year lease with proper credit score. If you find the right property though, with the right tenant, it can be a goldmine.

If it stands empty for months you aren’t doing it right. Most rental companies suck. I touch base with my tenants 6+ months out to see if they want to renew and start doing showing/interviews 6 weeks before the end of the prior lease. Longest I’ve had vacancy on 4 properties in 5 years is 1.5 weeks and that was more than covered by 1.5 month early lease termination fee (from money collected up front).

Gold has beaten the s&p the last ten years

Cash is an option – Federal Reserve Notes (or Swiss Franc notes, see your local Airport). Also the bank’s or credit union’s rating.

I’m mentioned precious metals but I expect Gold to go below 1200 before it does its moonshot.

When you don’t know, but things look chaotic, sometimes it is best to keep your powder dry and take a 0% this year until the flight path – up or down – is clear.

By the time the path is clear, its already had a 20-30% move in the direction its going. Just be diversified. Even 100% FRN or SFN is extremely risky. I like 30% domestic equity, 20% international equity, 20% commodities, 30% real estate personally.

Watch carefully and set stops.

The path can be clear when it moves 30% in the wrong direction. It is still a bet.

I work in Corp America. Not giving up 275k:yr to micro-manage my account.

The 275k/yr remainder you have invested can be decimated in a few microseconds of HighFrequencyTrading if you don’t micromanage.

HFT are mostly front-running for penny or fractions of a penny. Most of the flash crash issues have been fixed. Hopefully more trading will move over to IEX. And considering most of my equities are in ETFs, would be pretty difficult for them to “decimate” it.

“But stocks 8% is a dangerous myth. There were zero gains between 1966 and 1982 along with inflation.”

I learnt this the hard way. I’ve had 3 stocks go totally bankrupt and wish I had never heard about the goddamn stock exchange scam.

Keynes: In the long run we’re all dead – but he was gay so had not children so didn’t have to worry about grandchildren living in a nightmare dystopia.

TZ’s corollary: In the long run, all stocks to go zero (as do Fiat currencies).

Something always displaces companies. GE, if it is still in the DJIA is the ONLY company there that was there in the 1930s and it will likely blow up as it is more of a financial engineering company than one that produced the tech marvels it was known for.

The Dow indexes – Industrials, Transports, and Utilities, consist of a fixed number of companies. They started in 1896. See which companies were in the index over each decade.

Or look for “Survivor Bias” – companies are delisted often.

Correction. The odds bet at casinos are the best bet because the house has no advantage. It’s a dice roll.

The odds are in the houses favor 7:5. This is a pretty well known thing actually. If it were even Steven then there would be no profit in owning a casino.

The problem is, most people are too stupid to follow the buy and hold long mantra popularized by value investors. Even people who claim to have a long-term strategy will dump their shares at the slightest hint of bad news, allowing scudsuckers like Goldman Sachs and hedge funds to make a killing on a small market decline.

We always put in a call to our financial advisor to buy more when the market takes a huge dive. Never, EVER, sell on a downturn, instead, buy more. The market always rebounds. It rebounded after 1921, it will rebound on the next fall. Buy, hold, and buy some more.

A great follow up article would be Roth vs. Traditional 401K. Also interesting would be discussion on Taleb’s Barbell Strategy and allocating 20% of portfolio on more exotic investments like options or mineral penny stocks.

The reality is that most people will not be able to accumulate this level of wealth due to a combination of factors that reflect on the kind of world that we live in.The reality is that most people do not have the intelligence nor the desire and will power to be able to save most of their paycheque but would rather spend and waste it in the most ridiculous ways in order to stimulate and fulfill their short pleasures and desires.

Also, you must take into consideration the number of people in society that decided to make lifestyle choices that clearly exceeded what they can earn in a given year. These kind of choices include having kids and buying homes that will take over a decade or longer to pay off. The reality is that most people simply do not have the means to save and invest as a result of the price tag attached to these above examples and will simply have no choice but to spend their money rather than save and invest. The percentage of society that is living pay cheque to pay cheque has increased and the percentage of those who have a savings account has decreased.

Speaking of savings, have you observed the low and lousy rates of interests? Pathetic and will continue to stay stagnant or even worse, go into negative territory as we are seeing being implemented by many central banks around the world such as the ECB and Bank of Japan. Furthermore, factor in the fact that the central banks around the world have devised and ready to implement bail ins and more quantitative easings which will result in the value of your money to errode even further as well as rob you of your savings to bail out the bankers in the next banking catastrophe, and the end result that can be seen is that the banks do not want you to save but rather spend in order to stimulate an already failing economy.

Forget the banks, but the insane cost of living will tear a hole in your pocket as you try to make ends meet. For example, where there is actual work available in this disasterous service sector economy, the cost of living exceeds what most people earn. People end up having to fork over 80-90% of their pay cheque on just rent alone and with the price of even room sharing now going up, the concept of saving seems more remote than ever before. The reality is that is now becoming more of a tougher mission to save up cash and the entire system is rigged that way. While you work long hours like a slave, you end up giving that pay cheque to your slumlord, who is laughing his way to the bank.

I admire those who have the tenacity and the knowledge on how to save and invest. But let’s also be realistic as well. The old lessons handed down by baby boomers on financial matters such as “if you save now you can be a millionaire by the time you turn 65” is outdated and no longer reflects the real world or the kind of circumstances we find ourselves in. By all means save and keep doing so if you can, but at the same time, understand that markets can become volatile and crash at any time and bankers can rob you of your savings.

Simple solution: buy gold, silver, bitcoin and cash until interest rates rise. The economy is in a huge debt fueled bubble right now, but once the debts come due, money will flood into gold, and you can buy all the stocks and real estate that everyone’s selling.

That’s why I’m saving in hard assets until the crash. At that point, I’ll start investing in an index fund and benefiting from compound interest.

Imagine if you bought the vanguard 500 in 2009 when the price was as low as 31% of today’s price.

Interest rates will never ever ever rise substantially again

Borrowing money will never be expensive again?

Why not?

Theres no growth. Why would I lend you money at 8% knowing full well you will barely be able to pay it back at 4%?

Because after the economy crashes, there will eventually be a recovery. Why would I ever borrow from you at 8% when a bank will lend to me for free?

Things will change once the current regime runs out of money and their currency fails. That’s why you’re buying gold now, right? Bitcoin too 🙂

Bitcoins are not interesting anymore. They were interesting before they became interesting.

That wasn’t the point of my post, but…

Why don’t you find bitcoin interesting?

To be frank, I had not actually looked at the value of Bitoins recently. Seems it went up again.

Well, maybe I’m wrong, but here are my reasons:

1. The big rise in value is in the past. It was a big deal, but now I don’t see it doing another leap upward in comparable dimensions.

2. The danger of government regulation or even banning. Yeah, it’s decentralized, but who knows what those fuckers will come up with to ruin it for everybody. Technically, you have to pay taxes for those kind of transactions, but practically, likely nobody does. If I were a power-hungry politician, I’d do my best to illegalize it. Perhaps invent some bullshit story about a pedophile ring selling baby rape videos for bitcoins and thus demanding a ban or sth like that. Even if that does not eliminate Bitcoins, it is likely to affect the value a lot.

There’s no way to actually trace it to tax it or even effectively make it illegal. It’s literally without a fingerprint.

Yeah, the 2013 bubble was very exciting. I can see how price volatility might turn you off, but bitcoin is sound money like gold. It’s scarce and it has predictable rules and I find that incredibly interesting.

Bitcoin and gold could both be banned, but they’re also very difficult to control. I ain’t worried.

Of course. But GOJ, be more creative. Let’s play “If I was a fascist…”

For instance, you can – technically – easily force internet providers to install package tracing stuff on their routers or one day perhaps even force people to install surveillance software on their computers.

In fact, you would not even have to actually do it. If people believe that it is being done and that they run danger of being accused of some heinous thing and put away … they will just give in to fear and stop doing it. Not all, of course, but most of them.

Since I brought up the example … how many people do you think would even dare to search for child porn on Google? I know I don’t. I have no idea whether it is not all a big bullshit hoax and whether it actually exists in any significant amount, but I just don’t want to risk cops being at my doorstep again and putting me away.

Yeah, but how many people are actually into doing stuff that is forbidden? I can easily see how a few determined individuals will keep using it no matter what – but I don’t see how this will ever be something that the common sheepman does.

The price volatility does not scare me at all. I find it fascinating. It’s just that I don’t think it has a real big future in this world. May always stay a good method to pay for drugs in hidden online-marketplaces, but as an investment? Meh.

I don’t care what the idiots do. Regardless, I’ll use bitcoin and gold to store my wealth.

Bitcoin’s first major use was as the currency for silk road, but things have changed. The top use cases now are trading and wealth storage. Bitcoin isn’t used much for purchases.

Quite similar to gold in that way.

I don’t care whether people buy gold, silver or bitcoin. I just want the good people of this world to prosper despite the coming devaluations.

I get that, but whether normal people use them affects their value for investment. If they are used only for speculating, there is hardly real value behind them and you might just get another bursting bubble in the end, like with the housing stuff. Correct me if I am simplifying, though.

Normal people don’t have very much money, but you’re right. If the network grows and everyone uses bitcoin as money, each bitcoin will be worth many thousands of dollars.

However, there is no bubble in bitcoin right now. It’s only a $10 billion market. Bubbles are a result of hype and/or easy money. Bitcoin has neither of those.

Although I have a ton of hype and I expect to use bitcoin to grow my savings. Big time.

There was a hype in 2013. No guarantee it will not happen again. On the other hand, if it does, you can try to profit from it.

I didn’t think Bitcoin guaranteed privacy. I think it is semi-anonymous, but it lacks encryption. Maybe while you hold it, no one knows you have it, but when you actually use it for anything, your identity is announced. At least that’s how I understood it. I’ve been waiting for a more private, secure digital currency.

You can always scramble your communication. But yeah, I mean, if you use it to order a package of heroine to your home address, it is pretty hard to keep that secret.

You can change your digitial fingerprint on anything you receive, such that nobody knows where you got it from.

That’s certainly useful, but the thing that would get me to adopt digital currency was when my balance information was also private and secure, you know, the way the Swiss do it.

So encrypt your hard drive or device where you keep your e-wallet.

I’m more concerned with the powers that be knowing how much money I have, and where, so that it can be confiscated, ahem, excuse me, appropriated to better use.

If Bitcoin allows you to hide the *source* of income, but it’s still visible that you received $5,000 from someone, that’s not as valuable to me as obscuring the funds entirely. But perhaps I’m misunderstanding how it works.

Bitcoin DOES have a finger print – that is what the entire chain is. It has far more of a finger print than any other transaction, because you, personally, can examine the chain. This is obviously not the case with physical Sovereign issued currency, nor with credit card transactions.

It is also very easy to make it illegal. How do you buy bitcoins? Do YOU buy bitcoins? Are you going to your secret bitcoin dealer and giving him your gold shekels? Yeah, I didn’t think so.

That’s what I’ve been doing. Mostly silver and some gold. Right now silver is a bargain at $20/oz. When the QE bubble bursts and inflation hits, precious metals will soar. When interest rates begin to rise, the wheels are coming off of this thing. I really don’t mind inflation as long as wages keep up with it. I’d like to inflate my mortgage away.

Good point, I especially encourage investment in silver. Prices are very low right now. I should have sold mine when it hit $48 during the recession. I think you get more bang for your buck with silver but obviously diversify.

Retards have been claiming this bullshit for my entire life. How retarded can you be to write cogent sentences but believe such nonsense?

I will gladly argue with you if you have a point.

People not smart enough are not my problem. In fact, I hope that they stay poor. The less big money types, the further my dollar stretches since the economy will be balanced out at the average person’s spending level. That’s a great thing for me.

Capitalism – God’s way of determining who is smart, and who is poor.

This message brought to you by Ron Fucking Swanson. (click picture for enlarged view, its a great pyramid)

https://originaldave77.files.wordpress.com/2011/01/swanson-pyramid-of-greatness-nexus10-2560×1600.png

Yep. Capitalism is a mix of Darwinism and Economics.

I once got my chest hair shaved for a stupid minor operation. I never felt so humiliated. 🙁

lousy rate of interest is inversely proportionate to low rate of borrowing. Yes, interest blows. So buy property while they are essentially giving the money away. When I was younger You could put 10k in a US Savings Bond and reasonably expect 10-13% interest. So at 21 if you had saved your pennies and dimes while living on the cheap you could put a 10k nut into a bond at 13% with a 50 dollar monthly contribution compounded annually and when you were 41 you would have nearly 170k. If you found you could still get 13% you could double down with 100 of it and at 61 when you were ready to retire you would have 1.2m plus whatever else you had saved, invested etc with which you could tell society to fuck off.

If you couldn’t get a good interest rate it would necessarily mean that borrowing money is a lot cheaper so you could take your 170k and put a down payment on a 1m dollar property….in NYC that would mean, now, a 1.5 bedroom in a very nice area where your monthly expenses including your mortgage common charges and taxes would, if you shopped well, be roughly the same or less than living expenses would be anyway so you sit in your investment and work and save until you are ready to sell out.

Over 20 years you can, conservatively, figure on 300% and so after living and working and saving you sell your home for 3m and take that and whatever else you have and say fuck off.

It isn’t about smart and stupid (except at the extremes of brilliant and dumb ass) it is about paying attention and staying patient.

Who’s going to be able to pay 3X what the price is now in the future? At what interest rates and salary? You’re still going to need some place to live too after you sell.

Meanwhile you spent a couple decades living with a million plus in debt hanging over you. Debt which means you have to get up every morning and go to work to feed the financial system. That interest is going to consume your 3X profit considerably never mind the consequences of being in financial bondage.

Today stuff like bonds backed by sub-prime auto loans pay high single digits. I don’t even want to know the risk level for 13%. That’s got to be almost certainty that the borrower is going to collapse and not pay,

Amen, couldn’t have said it better myself.

My advice is to wait for hyperinflation- we’ll all be millionaires then

100 million pesos baby!

I think there was a 100 mil dollar bill in Idiocracy- instead of “e pluribus unum” on the bill it was “haulin’ ass, gettin paid”

never saw it, but funny.

really? come awn maine. ask one of the 88 cobblers by you about it- they will give you a breakdown

lol.

You know that on a block around the corner from me there is a video rental place. Seriously.

I am contemplating getting a membership just so I can tell people “I have to return some video tapes”

Hehehe funky! Afaik there isn’t even one in the whole country since 5 yrs or so. No music stores either.

In Japan they still have both which I found amusing, Japan is like a mix of retro and super high tech, they all use cash and fax machines but had internet and TV on their phone 10+ yrs ago etc.

http://www.yelp.com/biz/we-deliver-videos-new-york-2

seriously thinking about getting a membership just for the line.

Seems like a fucking awesome place! I loved my ritual every Friday going to the local video store, who, like this place knew what I liked and greeted me by name :-).

They would flag me down every time they had something new they thought I would like, and almost always it was 100% hit.

Damn, miss those times in that respect, even thoug I have to say Netflix is pretty good, and between that and torrents occasionally I am covered.

The only thing it doesn’t really give is that browsing the shelves and being able to tell a lot just by the cover condition and stickers.

I don’t know how they are in business. I have a friend who got drunk and walked in and was asking if they have whores in the backroom.

It does seem awesome until I realize that I have pretty much 100k movies and tv shows on external hard drives.

But yes, I remember going to block buster, grabbing 2 flicks and a bottle on the way home

I had a friend get married in Cabo.. at one point the mariachi band was wheeled out to make an announcement.. ONE MILLION PESOS! The threshold had just been passed, counting bar, hotel, food, etc. That’s around 50 grand, which is kind of ridiculous to spend on a wedding, but considering he was picking up the tab for everyone, it was relatively cheap.

Want to know the real trick to achieving a small fortune?

Start with a large fortune, and then get married.

*rim shot*

Thank you, thank you, I’ll be here all week. Tip your hostesses! Good night everybody!

Unless I’m struck by the muse or lolknee’s jumps in with a grand slam comment, I think you’re gonna win the internet today with that joke. I’m just not in a very funny mood today….bet it’s that damn chess game.

you ready bud…..I came here to whoop ass and chew bubble gum and I am all out of bubblegum

Issue the challenge, champ. I got my coffee.

you issue it. I am a moron.

You really need to get the app. MUCH more user friendly.

That’s odd, because when I used to play Chess it would put me in a very happy, chipper mood. Put the pep in my step for the day, you could say.

Set that one up for you really well, didn’t I?

Right?

hey typing my post below I just had nostalgia for 20 year savings bonds at 13%.

Figured I would share my memories with someone who remembers the same presidents.

Yeah, I read it. I remember when you could get 7% on a freaking CD. I mean can you imagine that now? 7% on a fucking CD? Only in the dreams of yesteryear.

I can actually remember the news reporting on when Jimmy Carter was attacked by a vicious swimming rabbit. Greatest news story memory *of my life*, bar none.

My bank’s best offer is 0.75%.

I was stunned and even went in to talk to a banker to make sure I was doing the math right:

“So you’re telling me if I invest a $1000, into a CD for a year, then I’ll only make like $2 in interest???”

“…..yeah……”

I had a CD at 7 or something. Ha. I don’t even look now. Bigger return on investment selling loose cigarettes.

I remember rabbitgate (not that they called it that back then)

https://en.wikipedia.org/wiki/Jimmy_Carter_rabbit_incident

that is right there with Bush 43 and the killer pretzel, Dukakis and that absurd tank helmet and dick Cheney shooting a guy in the face (the funniest part about that was the guy’s public apology to Cheney for getting his face in the way of his gun)

You can’t get more gangster than shooting someone in the face, then having THEM apologize to you!

It’s true, like him or not that is pretty fucking baller.

Also, is that Pei Mei?

Yes sir. The best part of the movie!

“like all Yankee women, all you know how to do is order in restaurants and spend a man’s money”…Lol

When I was a kid I had a CD at 14%. Yes. fourteen f’ing percent interest. That was in Volcker era. Now we are in the Greenspan-Bernanke-Yellen financial repression era where no matter how much you save you can’t make shit in interest. I literally made more money in interest as a college student.

This is our new slavery. To make it impossible to achieve financial independence without winning in the wall street casino. And it is a casino where HFT algos will front run you and insiders have more information than you do. The house always wins in the end. Best you can do is get the right timing for awhile and get the f out while you’re ahead, just like a casino.

OTOH inflation was very high too but contrary to popular belief it’s actually a good thing if you do things right. The trick was to borrow at a fixed rate to purchase cashflow producing assets. Inflation helped you melt away your debt (and the cashflows would quickly become positive) I really don’t know why some ppl lament fiat currency.

Because they are ignorant and believe that bank’s lend grandma’s savings and collect the spread between her savings account interest and the note interest. Banks have never lent money, really. They have always created debt from nothing, fiat currency or not. This wouldn’t such an issue but the bank creates the money it gives you from nothing, and then requires you pay back the face amount PLUS interest. So, we see, we require inflation simply to cover future interest obligations without resorting to more borrowing.

The only thing a gold standard does is fix exchange rates, it never has had any impact on domestic spending. Libertardianism is the biggest problem in The Right today.

So many clichés here. When interest rates were at 14% inflation was out of hand, that was the only reason why the Federal Reserve kept them so high.

It was never possible to get rich by putting your money in your bank and receiving soe interest. Blame the HFT!

The point isn’t to get rich. The point is to get a decent safe return. Rates should be free market. Without the fed money creation interest rates should be very high right now due to the lack of real savings.

Have you ever thought about rental properties?

http://f.tqn.com/y/uspolitics/1/L/l/R/83956989.jpg

Yes. Problem is where I live if a section 8 comes along and meets the property owner’s basic credit requirements a landlord can’t refuse them. This requires mandatory government classes that have to be taken at one’s own expense. Furthermore I already lost enough money on real estate. In another five years I might be back up even and I didn’t even buy at the peak but years before it.

that is assuming a very, very good lawyer.

huh? are you saying I shouldnt try the veal?

You should sir, indeed you should.

It’s the best in the city.

damn you- I know youre referencing a movie…I have no idea…Police Academy 2?

nope.

https://vine.co/v/OUVELmqxw6B

“I will now speak to lolknee in Italian.” via a vine

take the gun. leave the canoli.

The funny thing is that is essentially my job, only updated for a world with computers. I am a suit in the construction world.

MasterCard….. the look on his face when he grabs his neck….. priceless….

what is that little suffix you have on your name “check” nationalist?

It’s a check mark, with the word “Nationalist” next to it.

Heh.

It’s something I copy/pasted into my user name.

Have lots of daughters and marry them off to rich suitors

“Have lots of daughters and marry them off to rich suitors”

Man the delusional mojo is nicely up-amped on this thread.

Today a man has zero (0) say as a father, and most likely your daughters (as all daughters today) will latch on to violent penniless losers, or Islamic extremists.

“Today you have zero (0) say as a father…”

You speak from experience, or ignorance?

Just because you don’t know how to control a family, nor can imagine it, does not mean it doesn’t exist.

Like I said, the delusional mojo is up amped on this thread.

I’m not wanting to put you or anyone on the defensive – I’m merely saying that men have very little say in how his raising his daughter. This should be painfully obvious. And whatever influence he has pretty much gets cancelled out once she moves out.

Yes, the world is against the Christian father, specifically designed to corrupt his daughter, to teach her to hate her father, her people, her nation, her God, and ultimately herself. For a daughter to tell her friends that she loves her father, trusts his wisdom, and obeys his teachings is to laugh, if you’re hanging out with kids that weren’t home schooled. I have a friend with 4 daughters, 3 grown and married off, none went to college and each married a good man. They were successfully transferred from father to husband, to motherhood, without problem. They were home schooled and the parents lives a genuine, faithful, life.

I am definitely pleased to read this.

This situation is ideal. I wish more would do this.

The hostess will be getting more than a tip

She’ll have the full 3…. I mean 9 inches

The guy who made Grey Goose vodka and Jaegermeister popular, made his first money getting married. He said it was easier to marry a million dollars than it is to make a million dollars.

Another version of that joke goes:

Q: can a woman make a man a millionaire?

A: yes, if he’s a billionaire

The fastest way to become a millionaire is by first being a billionaire.

This article is out of date…. compounding interest….WTF… 1/2 worlds bonds have a negative coupon now……

I thought you were dead. Love your music, man.

Fastest way to becoming a millionaire; create refrigerator magnet with trite platitude.

Wow….. That wasn’t a rim shot, it was nothing but net. Hats off. But tip the hostess 15% not 20%, she knows the difference and she’ll get the message.

Interesting, but all of is only applies very selectively.

To give an example, a friend of mine used to take part in the retirement savings scheme of his employer who matched funds into it. He worked for 3 years and change but for the sake of argument let’s say 3 exact.

He paid 55€ per month into the fund, matched by the company in full for a total of 110€ per month.

So, after 3 years he should have 36×110€ + interest in it, we were talking about it and I told him to check the balance.

He came back the next day red in the face, his total balance was 300€ and change.

Throwing money into a black hole more or less.

My strategy is and has been for as long as I’ve had one is save nothing, and absolutely no investment funds etc. I’m the only employee where I work who has managed to get excluded from the pension plan (I was part of the team who negotiated the current agreement with the bank on behalf of the company).

Further, I don’t think that even if there was a reasonably lossless way to save that any of that would ever benefit me. I doubt seriously that governments the world over will not have taken everyone’s pensions one way or another by the time it would be relevant for me, which seems to be around 74 if I live that long.

Actually I think it will happen much much sooner.

I think the best thing to do if you are serious about it is to follow your gut and see the next big thing coming before it becomes a big thing. Invest in that.

Like, had you invested in Bitcoins a decade ago (not sure if it already existed) merely 1000€, you would be rich by now.

Yeah you could have done like me and mined the shit out of bitcoins on free power and sold them when they were $1000/btc.

Heh I literally junked my miners after they got slow, which was if memory serves me 18month max from when they were delivered new. They cost I think a bit over $1000/pcs but mined several whole bitcoins on average over that time span so it was a pretty good net win.

I had lots of miners, I’m trying to remember exactly but I think 12 at most, they were several different price classes, the above $1000 one is an example.

Think mining would still have a little pay off today?

Unlikely. The cost of electricity to run the rigs big enough to get even a marginal return on BTC is huge now.

Highly dependent on how much you pay for electricity. If it’s free or industrial price sure, even with old miners. But you can actually calculate this, it’s just pure math.

You factor in the total cost of your mining setup, plus the cost of power to run it a year for example, then you can also calculate quite closely how many Bitcoin or fractions of btc it will generate over that time with the difficulty increase projection taken into account.

There are online calculator sites for this, but double and triple check before spending money, and never buy a miner that you have to pre order. Take my word on this one, it will save you a lot of headaches. Buy only miners that you can take physical delivery of and see running within 24hrs or so, otherwise you’ll lose the most productive mining time.

It’s harsh and hard but if you have the balls, money, opportunity of cheap power and commitment you can make money still today.

Pro tip, monitor all your miners all the time, they sometimes need a restart or other attention and downtime means direct loss of income.

You forgot:

Risk of Nationalization.

Soon to be coming to the US, brought to you by the SEIU.

Two Scenarios:

1. Your retirement accounts will be nationalized to provide a “shared retirement”, and objectors will be shamed and penalized for being evil and greedy.

2. You will be required to hold 50-75% of your retirement account portfolio in “US Government Retirement Bonds”, which will be indexed to inflation to provide 3% returns.

Investing in retirement accounts at the pinnacle of stock market bubbling is POOR investment advice. Expect 3-5% returns if you do, and understand that you are fucking hogs to be slaughtered.

Want investments? Invest in Russia. Invest in small technology like 3d printing, robotics, space exploration. Buy a business, start a business, and employ only yourself.

Just think of the nationalization of gold in bank accounts … don’t remember where that was.

My grandfather in Czech used to own a garage with lots of equipment for building motors etc. When the Soviets came and took over, the bastards took it all away.

@disqus_q7cnnyJ7N9:disqus just remember https://uploads.disquscdn.com/images/cc96dd8c1f50f0373d990974a5c7d52dd20732152f2c8a4dd6ce6edc4365e8c5.jpg

Go fuck yourself, cunt. Heh.

it’s the gift that keeps on giving.

Obviously you played a complete amateur.

Ouch…Damn….that’s gonna leave a mark…

Nah. You have to have a brain, soul and Dick to have any sense of reality.

If it was from anyone else, maybe.

dude, go crawl under a rock. You aren’t even fun stupid…just stupid stupid.

Idiot but with NM chess rating. What’s yours?

I dare not ask about your opponent’s? LOL

yawn. Keep bragging about acolytes. I am sure you are also a black belt and have a 10 foot dick. In the end the truth shows through. You are weak and foolish and boring.

Leave it to some cunt on the internet to take a joke of one bad chess game and turn it into a dick measuring contest. Are you quite finished?

Oh, so it was you! You must have been drunk or blind or both.

Anyways, it’s a cheap win, so don’t feel too bad about it.

Sometime you win, sometimes you lose, sometimes you just totally fuck it up.

True I’ve had some silly games in my time but to boast about such a cheap win is stupid.

He’s not so much boasting as just shit talking about my stupid move. Normally our games are a real slug fest with most of the board being wiped clean. It’s all in good jest. I trigger him with pictures of camping all the time, the dear city slicker.

Still my comment stands.

he doesn’t even see the silly move. He has no idea what is going on. He is trying to be something he isn’t —- not an idiot.

still? everything you say is stillborn.

So it was a cheap win, why brag about it?

Shut up moron

Answer the question! … LOL

You really are fucking stupid. I mean, good luck man.

Because they’re buddies and lolknee was busting his chops as a joke. This is how men goof around, they give each other shit. If you get any male friends in the future, you should give it a try. It’s no end of fun.

And decides to post it on a forum full of mostly strangers? Makes no sense.

Inside jokes are for inside consumption.

Most regulars here know each other and communicate here and off this site in ways you clearly are ignorant about.

Give it up and walk away. You’re out of your league here.

It’s sad reading about a 15 yo who thinks about pension.

I invest in my children and in my health. No plans for retirement. When I feel that the body is totally useless to keep me, I’ll just disappear in the woods and die like an wounded wolf.

So the minute you get sick, you’ll be kept on the public dole on my penny, or you’ll wander into the woods and I’ll be stuck with the tab of burying your half eaten corpse. Great. Thanks.

A wise man understands that planning for the future beats relying on chance any day of the week. Working until I’m 101 because I didn’t plan sufficiently to be comfortable in my old age would *fucking suck*.

no he wants to die like a wounded wolf….which, coincidently, is exactly how the bums who eat what I throw away die.

I’m not made of steel and I do get sick but always manage to fix myself – it’s a field which I’m highly involved. When it gets to the point of no return, I’ll head for the woods.

You act as if you get to choose the time and way by which you become helpless. I watched my father in law die of a disease that allowed him no such “walk into the woods” option, instead giving him a “waste away in bed as your limbs are sawed off” option.

Your failure to plan is going to cost me money. Just more inspiration to trash Obamacare and socialized medicine now, before suckers like you get old and cannot take care of yourselves.

Hey Kasparaov, watch out for mental illness. You may not see it coming but I do.

Don’t give him too much advice. The world needs people to pump gas and the such.

You don’t worry about that I know what I am doing, I know how to read the signs of the body plus we’re not in the same neck of woods so don’t lose any sleep over it.

Yeah, sure you do. I can tell by your excellent ability to grasp unknown variables and conclude that you have it under control.

Whatever happens to you, is your business. As long as I don’t have to pay for it or participate.

This is exactly why I deplore Obamacare and socialized medicine. I want people like this guy to be able to make that choice without compromising others.

Exactly. It forces them to plan, or accept the consequences of monumentally stupid choices.

Yup. I want people to be able to make stupid decisions without feeling “the hive” making them feel guilty for it as if we were one fucking collective consciousness type thing like the Borg.

that Is very wise mr arrow. a very wise comment. The sad thing is that this dumb shit is going to be leeching off of the money I make, money I could be saving for an earlier retirement.

Obama Flowers

Receptionist: Hello, Welcome to ObamaFlowers, My name is Trina. How can I help you?

Customer: Hello. I received an email from Professional Flowers stating that my flower order has been canceled and I should go to your exchange to reorder it. I tried your website, but it seems like it is not working. So I am calling the 800 number.

Receptionist: Yes! I am sorry about the website. It should be fixed by the end of November. But I can help you.

Customer: Thanks, I ordered a “Spring Bouquet” for our anniversary, and wanted it delivered to my wife.

Receptionist: Interrupting, Sir, “Spring Bouquets” do not meet our minimum standards; I will be happy to provide you with Red Roses.

Customer: But I have always ordered “Spring Bouquets”, done it for years, my wife likes them.

Receptionist: Roses are better, sir, I am sure your wife will love them.

Customer: Well, how much are they?

Receptionist: It depends sir, do you want our Bronze, Silver, Gold or Platinum package.

Customer: What’s the difference?

Receptionist: 6, 12, 18 or 24 Red Roses.

Customer: The Silver package may be okay, how much is it?

Receptionist: It depends sir, what is your monthly income?

Customer: What does that have to do with anything?

Receptionist: I need that to determine your government flower subsidy, then I can determine how much your out-of-pocket cost will be. But if your income is below our minimums for a subsidy, then I can refer you to our FlowerAid department.

Customer: FlowerAid?

Receptionist: Yes, Flowers are a right. Everyone has a right to flowers. So, if you can’t afford them, then the government will supply them free of charge.

Customer: Who said they were a right?

Receptionist: Congress passed it, the President signed it and the Supreme Court found it constitutional.

Customer: Whoa! I don’t remember seeing anything in the Constitution regarding flowers as a right.

Receptionist: It is not really a “Right in the Constitution,” but ObamaFlowers is Constitutional because the Supreme Court Ruled it a “Tax”. Taxes are Constitutional. But we feel it is a right.

Customer: I don’t believe this.

Receptionist: It’s the law of the land sir. Now, we anticipated most people would go for the Silver Package, so what is you monthly income sir?

Customer: Forget it, I think I will forgo the flowers this year.

Receptionist: In that case sir, I will still need your monthly income.

Customer: Why?

Receptionist: To determine what your ‘non-participation’ cost would be.

Customer: WHAT? You can’t charge me for NOT buying flowers!

Receptionist: It’s the law of the land, sir, approved by the Supreme Court. It’s $9.50 or 1% of your monthly income.

Customer interrupting: This is ridiculous, I’ll pay the $9.50.

Receptionist: Sir, it is $9.50 or 1% of your monthly income, whichever is greater.

Customer: ARE YOU KIDDING ME? What a rip-off!

Receptionist: Actually sir, it is a good deal. Next year it will be 2%.

Customer: Look, I’m going to call my Congressman to find out what’s going on here. This is ridiculous. I’m not going to pay it.

Receptionist: Sorry to hear that sir. That’s why I had the NSA track this call and obtain the make and model of the cell phone you are using.

Customer: Why does the NSA need to know what kind of CELL PHONE I AM USING?

Receptionist: So they get your GPS coordinates sir.

Door Bell rings followed immediately by a loud knock on the door

Receptionist: That would be the IRS sir. Thanks for calling ObamaFlowers. Have a nice day and God Bless America

this, by itself, could be an ROK article. no other comments necessary.

Just to give due credit to the author: http://www.activistpost.com/2013/12/the-obamaflowers-spoof-parody-on.html

Unknown variable: You get hit by a car tomorrow and all your attempts to plan for the future will become obsolete.

Que Sera, Sera.

So your plan is, don’t plan.

Great thinking, Scooter.

Better to plan and not need it, than need it and not have planned previously.

Your financial knowledge and skills are clearly sub par and unrealistic. I’m glad that I won’t have to pay for your poor decision making, I’ll tell you that much.

Alternate plans are quite possible hehe. I don’t have a retirement plan because they are net losses of money, what I do have instead is stuff that keeps going up in value, mostly ridiculously rare items that by now most would sell to a museum or collector quite fast. Not stuff I use or have sentimental attachments to, simply stuff I bought and usually got very good deals for, for the time when I bought them, and that now are much more valuable.

To give one example which cost me very little, I have the fastest possible true 486 PC possible with normally available parts of the era.

There simply were never components better made than the ones I have.

Yes of course it runs MS DOS 6.12 etc, but it has 128mb 60ns FPM, Matrox plus SLI Voodoo 2 graphics, SB AWE32.

The CPU is this https://en.m.wikipedia.org/wiki/Am5x86

Yes I know nerdorama but I think you know what I’m talking about.

Do you think all the great explorers in the past were thinking about retirement when they sailed towards the unknown horizon?

Today, we live a in very unadventurous, stale society, hence we make no great discoveries anymore.

p.s. Have you already bought your plot in the cemetery too?

Dude, I’m giving you the “out” so that you don’t have to keep making me point out your utterly stupid “retirement planning” strategy over and over again. Be wise enough to at least take the “out” gracefully.

Let me guess. Neckbeard with a comic book collection?

Nope, have beard yes but trimmed and proper, no comic books, not even one in my home. The other things I have are mostly antique books, among them a bible printed 1776. There are 7 of them known in museums and 2 privately owned counting mine.

Edit: should add I’m married and quite successful with the ladies lol.

man, you have said some dumb things in these here comments sections but this takes the cake.

Number one advice is to get out of debt. Any payment to the principle is a guaranteed return on the interest (almost due to tax deductible mortgage interest, etc.).

A savings account??? Ok I can see the point of get the fuck outta here money, or saving for a house, etc. Even buying a house I wouldn’t advise at the moment. I’m toying with the idea of buying a Dutch Barge. No property taxes, moveable to a certain extent, and it is a sure way to get her knickers wet.

Interest rates at the moment have tanked. The banks are giving nothing and in some instances are throwing around the idea of charging interest on their customers money.

Compound interest only works when the bank wants to hold onto your money. 10% interest on deposits haven’t existed in 20 years……

What happens when the entire banking system goes belly-up?

I can’t even think about investing anymore, somehow I think WWIII is going to change the equation.

What if a meteor hits the earth and kills everyone? Tomorrow is never guaranteed but that shouldn’t deter your from investing. If you’re worried about the entire system collapsing, be sure to also invest in other things like silver/gold, ammo, food, etc.

Land and forestry also……

Ammo & guns – but fuck the market, CDs 401K, and all the other blue pill crap

That “crap” isn’t blue pill. CD’s are, ok, sure, they’re silly. But investments, and 100% employer match to the first 6%, are pretty damned nice. So is the market in general, if you know what you’re doing.

You’re telling me I can’t climb to financial success on a CD ladder?! I’m shocked! /s

I know, right?

Yes. I get 100% employee match fund. Nothing blue pill about free money.

Or…nothing will happen and, by failing to invest out fear of potential events that never occurred, you’ll find yourself old and working bus on tables until you die.

I hear ya gof, but I think investing in hardcore stuff like precious metals and ammo would be better than the standar 401k.

Not gonna get any interest on those bars of gold and bullets. By all means, buy them, but also have monetary investments as well.

Turns out, you can do both. I have pounds of actual real life silver, and some gold too, in my gun safe. Which also alludes to the notion that I collect firearms and ammo.

But are you storing the most important thing of all?

Love? Yes, I have a giant Hug Box where I place all of my love and tender feelings every single night!

I meant Kratom, but it can certainly substitute for a hug box. It can substitute for anything.

But Unabashed….Kratom IS Love.

Hippie queer

You don’t understand that currency and the banking system is a function of sovereign power. The banking system doesn’t go belly up just like sovereign issued currency doesn’t go belly up, except when the ruling sovereignty ceases to wield political power, usually by external conquest but sometimes by subterfuge.

I think I get what you are saying – can you put this in more laymans terms? So you are saying that the system if bank8ng never really dies out?

File a civil lawsuit against any cunt who disparages you. If she writes bad shit about you on Twitter or Facebook (or anywhere else), sue her for libel. If she says bad shit about you to anybody else, sue her for slander. With all the man-bashing women do these days, it just might turn into one hell of a profitable hobby for us men. (And just imagine it – instant female accountability. What an interesting way to drag women into the daylight, so everyone can see them for what they really are. And it just might make the cunts think twice about their words and actions, too…win/win.)

My initial reaction to that is the “white knight” male judges, and female judges, would nip that in the bud.

I thought the same thing initially. And you could be right. But it’s all about proof. If you have the tickets to win, you have the tickets to win. If a cunt shoots her mouth off, all of her friends will read it. If you’re the guy on the end of the rant, and she was lying, you’ve been damaged – which proves malice. Make every cunt prove in court that what she says, or writes, is true. Most of them lie about all of the myriad shit that allegedly happens to them at the hands of men, so that part would be easy…but yeah, certain judges might try to shoot it down. It sure would be worth a shot though. I read articles here at ROK frequently, but very few give you practical ways to get retribution and/or recompense in your dealings with malicious cunts. I think we should start hitting them where it hurts most – in the pocketbook; and, tangentially, their precious little faux reputations…

I think your head is in the right place. But how do you plan on dealing with the flood of tears in court. Like “He said this…boo boo…Then he did that…boohoo… ” don’t you know she’s always the victim? You ever watch any of those judge shows, it works every time. Female privilege.

I think it depends on the situation. If you have proof, that’s the first important thing. Secondly, you need witnesses who can attest to princess’s penchant for being a liar. And they should be pretty easy to round up. Also, during the discovery phase, you would undoubtedly find other men whom princess has fucked over. And they will no jump at the chance to testify to her lack of character, and spell out exactly what a cunt she is. I guess it all depends on how far a guy is willing to go. Now, me, personally, I won’t put up with any shit from a woman. I always get even – and then some. If more guys stood up and taught princess a lesson, princess wouldn’t pull her usual shit. When I hear stories from men about how women fucked them over, I always ask them, “What did you do about it?” And they usually just shrug, like, what could I do? If the courts don’t give you satisfaction, create your own. I once videotaped this whore I was living with, by hidden camera, while she was fucking a guy in our bed (a black guy). I sent copies to everybody she knew – including the manager at her local grocery store, her dentist, her employer. I mean I sent them to everybody, her mom and dad included. She wound up having to leave town. Don’t let them get away with their bullshit. If more guys retaliated in this manner, more women would refrain from pulling their usual cunt stunts. I guess that’s the whole point – get even with them, don’t take it lying down – get satisfaction in a court or elsewhere…

Good suggestions, but without the two main principles, hard work and discipline, its all for nothing.

Worked fine in the good old days when investment markets were not as rigged as they are now. Now, with the central banks pouring on “zero interest rates”, you can’t save and gain interest; you have to risk everything in the stock market, which is clearly rigged against the small guy. Start a company instead.

with you until the last four words.

Starting a company is entering into a rigged market as well. The bigs and insiders have all the regulation set up to smash new comers. The only place worth starting a company is in some business that isn’t regulated.

Hell, just start a GoFundMe account, like this ex-porn star did:

https://www.gofundme.com/8i0z3o

Her stage name is Carmella Bing.

Poor baby. Her life was ruined, and she needs to get her truck out of hock, so she can get her child back! Looks like she got more than her target goal of $700…

Who knew making money could be so easy? Spread your legs, fuck a couple of hundred monster cocks on camera, hit the wall – and then ask for donations on GoFundMe. The betas will line up.

Sick shit…

Carmella Bing was a top porn star back in the day. Last video I saw of her she got ridiculously fat though.

Women are horrible with money management. Carmella had to have been making great money in porn, but it’s ridiculous to see that she now has nothing.

If you’re going to be a whore, at least have something to show for it

Agreed.

A lot of ex-porn stars turn to escorting – but Carmella’s way too fat to pull that off. Thus, she’s shilling for GoFundMe money. She actually creates halfway-decent artwork, too. Nice angle there. Sell your paintings to desperate betas who think they’ll get a chance to fuck you after the sale.

But yeah, it’s ridiculous that these porn sluts can’t save money. Most of it is probably spent on drugs, or on buying their latest skeezy boyfriend a Harley – shit like that.

I met this porn star at a strip club a couple summers ago. We spent about an hour talking. She asked for my cell phone number. So I gave it to her (mostly so I could show it off to a couple of friends). She called me off and on, all day long, over the next couple of days – but I didn’t answer. I know I could have banged her but after thinking about the countless cocks that had been buried in her oft-used holes, I passed. (Plus, she was fucking insane – daddy gave her too many hugs, most likely.)

Last time I checked, she was out of the porn business and was working as an escort. (What a shock!) I might have to text her and tell her to start a GoFundMe page…

“Women are horrible with money management.”

The worst. There was a very attractive local hooker (never spent time with her myself btw), who, in her prime, was making over $200k/year. She had one man who would book her for an overnight visit once a week at $1,000, $52,000/year from one john.

Looks and body started taking a turn for the worse a few years ago. Phone stopped ringing. Her weekly john found someone younger/prettier/better body.

Her money management was so awful that she took a job bussing tables at some greasy spoon restaurant to make ends meet. Money just slipped through her fingers like sand…

Looks like I’m being called to Turkey…. to the Bat cave!……erm……to the Cave!

This is sucker shit.

The real way to become a real-deal millionaire is to take chances. Period. Your retirement account can get wiped out. Wages are declining. You will most likely need to strike it big if you want to get into 8 figure territory.